I was reviewing a cost sheet with a brand owner from Chicago last month. She was launching her first summer coat collection, a beautiful linen-blend trench coat with a partial lining, custom buttons, and a self-fabric belt. She had budgeted $18 per unit based on a quotation she received from a factory on Alibaba. The factory had quoted $12 for the coat itself, $3 for shipping, and $3 for "miscellaneous." She thought she had a $30 margin at her planned $48 wholesale price. I asked her to walk me through her landed cost calculation. She stared at me blankly. "Landed cost? The factory said $18 per unit delivered." I opened my laptop and built the real cost model with her. The actual landed cost was $26.80 per unit. Her $30 margin was actually $21.20. Her profitable collection was barely breaking even after marketing spend. The Alibaba quotation had excluded import duties, customs brokerage, port handling, and the 3% Trade Assurance fee. The factory had not lied. They had simply not mentioned the costs that were not their responsibility under FOB terms. The brand owner had filled in the gaps with optimistic assumptions. The gaps consumed her margin.

The true cost of manufacturing a women's summer coat is composed of seven distinct cost categories: fabric cost, which accounts for 35% to 45% of the total FOB cost, trim and component cost at 8% to 12%, cutting and sewing labor at 18% to 25%, factory overhead and margin at 12% to 18%, quality control and testing at 2% to 4%, shipping and logistics at 8% to 15% of the total landed cost depending on mode and volume, and import duties and customs fees at 15% to 28% of the FOB value depending on the HS code classification and the country of origin. A medium-complexity women's summer coat with a linen blend shell, partial lining, and standard trims typically has an FOB cost between $16 and $24 and a total landed cost at a US warehouse between $22 and $34 per unit.

Understanding the true cost breakdown is not an accounting exercise. It is a margin protection tool. A brand owner who does not understand where costs originate cannot negotiate effectively, cannot identify cost-saving opportunities, and cannot build a retail pricing model that survives the reality of international logistics. At Shanghai Fumao, I provide every prospective brand partner with a transparent cost breakdown. I want our partners to understand their costs because a partner who understands costs is a partner who prices profitably, grows sustainably, and re-orders consistently. Let me walk you through every component of the cost structure, with real numbers and real examples from our production floor.

The FOB Cost: Fabric, Labor, and Factory Margin

The FOB cost, Free on Board, is the price the factory charges to produce the coat and deliver it to the port of export. It includes all raw materials, all production labor, all factory overhead, and the factory's profit margin. It does not include ocean freight, insurance, import duties, or destination charges. The FOB cost is the foundation of the landed cost calculation. Every other cost component is calculated from or added to the FOB value. A mistake in the FOB estimate propagates through the entire landed cost model. The FOB cost is determined by four factors: the fabric consumption and fabric unit price, the trim and component cost, the sewing labor time and labor rate, and the factory's overhead allocation and profit margin.

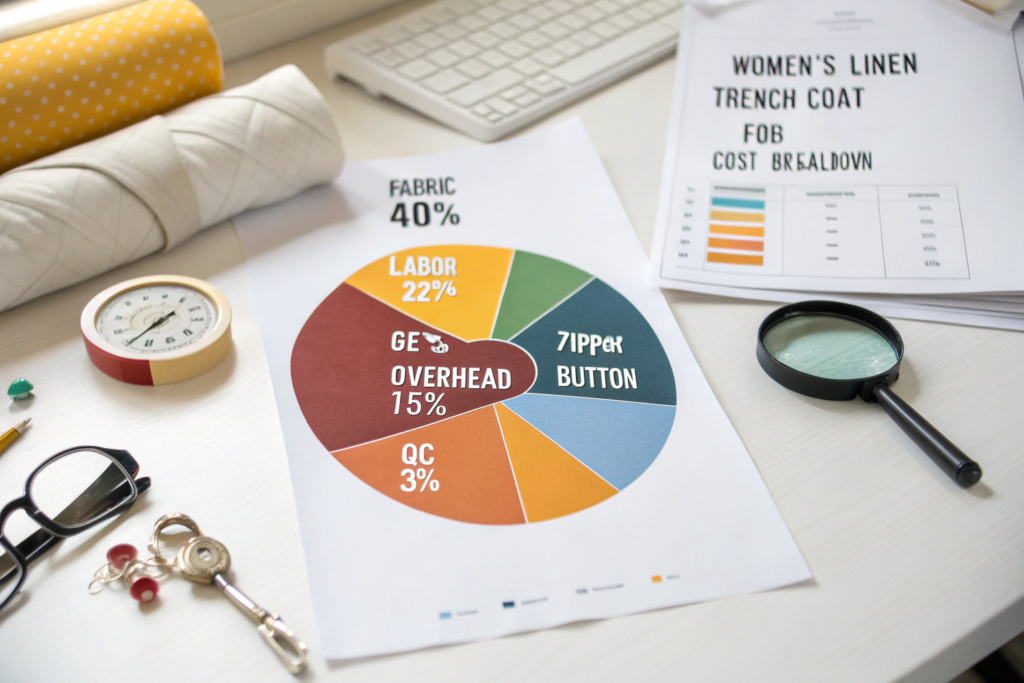

For a representative women's summer trench coat in a medium-complexity design, unlined or partially lined, with a cotton-linen blend shell, standard polyester buttons, and a self-fabric belt, the FOB cost breakdown is as follows. Fabric: the coat consumes 1.8 meters of shell fabric at $5.50 per meter, totaling $9.90, plus 0.8 meters of lining fabric at $2.20 per meter, totaling $1.76. Total fabric cost is $11.66. Trims: buttons, thread, labels, hangtags, and polybag total approximately $2.50. Labor: the coat requires 65 minutes of standard allowed minutes for cutting and sewing. At a labor rate of $0.12 per minute, which reflects a skilled operator wage in a Chinese factory plus social insurance and benefits, the labor cost is $7.80. Factory overhead and margin: overhead including electricity, equipment depreciation, factory rent, and management salaries, plus the factory's profit margin, is approximately 18% of the sum of fabric, trims, and labor, totaling $4.00. The total FOB cost for this representative coat is $25.96. This is a realistic, transparent FOB cost for a medium-quality, medium-complexity summer coat produced in a compliant Chinese factory.

The fabric cost is the largest single component and the most variable. A coat made from a premium European linen at $8.50 per meter will have a fabric cost of $15.30, an increase of $5.40 over the standard linen blend. A coat made from a basic polyester chiffon at $2.80 per meter will have a fabric cost of $5.04, a decrease of $6.62. Fabric selection is the most powerful cost lever available to the brand owner. The labor cost is the second most variable component. A simple open-front kimono with no buttons, no lining, and French seams might require only 35 minutes of sewing time, reducing the labor cost to $4.20. A complex belted trench coat with epaulettes, storm flaps, buttonholes, and a full lining might require 95 minutes, increasing the labor cost to $11.40. The design complexity directly determines the labor cost. The factory's overhead and margin percentage varies by factory type. A large, high-volume factory with automated equipment may have a lower percentage but a higher minimum order quantity. A smaller, more flexible factory may have a higher percentage but lower minimums and more personalized service.

How Is Fabric Consumption Calculated for Costing?

Fabric consumption is the amount of fabric required to produce one coat, including cutting waste. It is calculated by the pattern maker using marker making software. The software arranges the pattern pieces on a virtual fabric width to minimize the space between pieces. The total length of fabric required for one complete set of pattern pieces, plus the unavoidable space between pieces, is the fabric consumption per unit. The consumption is affected by the garment size, with larger sizes consuming more fabric, the fabric width, with wider fabric allowing more efficient pattern placement, the pattern complexity, with more pieces and more curved seams generating more waste, and the fabric pattern or nap, with one-directional prints or fabrics with a nap requiring all pattern pieces to be placed in the same direction, increasing consumption by 8% to 15%. The standard practice is to calculate consumption for the middle size, typically size medium, and apply a size-weighted average if the order includes a range of sizes. The cutting waste, the fabric that is cut off and discarded, is typically 3% to 8% of the total fabric laid on the cutting table. Efficient marker making reduces waste. Inefficient marker making increases it. The fabric consumption figure on the cost sheet should be the actual calculated consumption, not an estimate. An estimate that is 10% too low results in a fabric cost that is 10% understated and a total FOB cost that is 3% to 4% understated.

What Is a Reasonable Factory Margin for a Summer Coat Order?

Factory margin is a sensitive topic that is rarely discussed transparently between buyers and factories. The factory must earn a margin to remain viable. A factory that does not earn a margin will cut corners on materials, underpay workers, defer equipment maintenance, or eventually close. A reasonable factory margin for a summer coat order from a compliant, quality-focused Chinese factory is 8% to 15% of the total FOB cost, expressed as a markup on the combined cost of materials, labor, and overhead. This margin covers the factory's business risks: order cancellations, quality claims, currency fluctuations, and the cost of capital tied up in raw material inventory and buyer receivables. It also funds reinvestment in equipment, training, and facility improvements. A factory that quotes a price with a margin below 8% is either operating with extraordinary efficiency that its competitors cannot match, which is possible but rare, understating its true costs and planning to recover margin through change orders or hidden fees, or cutting costs in ways that will affect quality or compliance. A factory that quotes a price with a margin above 20% is positioning itself as a premium provider and should be able to demonstrate corresponding premium value in quality, speed, or service. The margin is not a fixed percentage across all orders. A large order of 1,000 units may carry a 10% margin because the fixed costs are amortized across more units. A small order of 200 units may carry a 15% margin because the fixed setup costs represent a larger percentage of the order value. This is the economic logic behind minimum order quantities and small-order surcharges.

The Hidden Costs: Shipping, Duties, and Destination Charges

The FOB cost is the price of the coat at the factory door. The landed cost is the price of the coat in your warehouse. The difference between the two is the hidden cost cascade that surprises first-time importers and erodes margins. The hidden costs fall into three categories: international freight, import duties, and destination charges. Each category is a function of the FOB value, the shipping mode, the HS code classification, and the port of entry. Understanding these relationships allows you to predict your landed cost with accuracy and to make cost-saving decisions such as choosing a lighter fabric to reduce freight by weight or selecting an HS code with a lower duty rate.

The hidden cost cascade for a representative summer coat with an FOB value of $25, shipped by ocean freight from Shanghai to Los Angeles in a less-than-container-load consolidation, is as follows. Ocean freight: the coat weighs 400 grams and occupies 0.008 cubic meters when packed. At an LCL rate of $120 per cubic meter, the freight cost is $0.96 per coat. At a weight rate, if applicable, the cost is similar. Marine insurance at 0.5% of the FOB value is $0.13. US import duty at 27.7% of the FOB value, the current rate for women's woven cotton coats from China including Section 301 tariffs, is $6.93. Customs brokerage at a flat rate of $200 for the shipment, spread across a 500-unit order, is $0.40 per coat. Destination port handling, terminal fees, and documentation charges, approximately $400 for an LCL shipment, is $0.80 per coat. Drayage and final delivery to a local warehouse, approximately $500 for a consolidated load, is $1.00 per coat. The total hidden costs are $10.22 per coat. The total landed cost is $35.22 per coat, which is 41% above the FOB cost.

The duty rate is the largest single hidden cost and the one that most dramatically impacts the landed cost. The 27.7% rate is the sum of the standard MFN rate, typically 19.7% for woven cotton coats, and the Section 301 additional tariff of 7.5%. This rate applies to the FOB value, not to the FOB plus freight value. A $25 FOB coat pays duty on $25, not on $26. The duty is calculated by the customs broker and paid to US Customs and Border Protection at the time of entry. The duty is a pass-through cost. The factory does not control it. The factory does not profit from it. Under DDP shipping, the factory pays the duty and includes it in the DDP price. Under FOB shipping, the buyer pays the duty directly through their customs broker. The duty rate varies by the fiber content and the garment type. A women's cotton coat has a different rate than a women's synthetic fiber coat. A coat classified as a windbreaker has a different rate than a coat classified as an overcoat. Correct HS code classification is not just a compliance requirement. It is a cost management tool.

How Can You Estimate Your Landed Cost Before Placing an Order?

The landed cost estimation formula is straightforward if you have the correct input data. The formula is: Landed Cost equals FOB cost plus Ocean Freight per unit plus Insurance per unit plus Duty, which is the FOB cost multiplied by the applicable duty rate, plus Brokerage per unit plus Destination Charges per unit. The FOB cost is provided by the factory quotation. The ocean freight rate is provided by the freight forwarder or, under DDP, is included in the factory's DDP quotation. The duty rate is determined by the HS code classification of the specific garment. The brokerage and destination charges can be estimated based on the shipment size and the port of entry. For a small-to-medium brand importing 300 to 800 units, a reasonable estimate for brokerage and destination charges combined is $2.00 to $4.00 per unit for LCL ocean freight. For a full container load, the per-unit cost is lower, typically $1.00 to $2.00. The most common estimation error is using an incorrect duty rate. I recommend that every brand owner obtain the correct HS code for their garment from the factory or from a customs broker, verify the duty rate on the USITC HTS website, and use the verified rate in the landed cost calculation. A second common error is forgetting to include the cost of the customs bond. A single-entry bond for a shipment valued under $100,000 costs approximately $50 to $100. A continuous bond for multiple shipments over a year costs $250 to $500. The bond cost per unit is small, typically $0.10 to $0.30, but it should be included in the landed cost for complete accuracy.

What Is the Cost Difference Between Ocean and Air Freight for Summer Coats?

The choice between ocean and air freight is a trade-off between cost and speed. Ocean freight from Shanghai to the US West Coast costs approximately $0.50 to $1.50 per coat for LCL shipments, depending on the coat's packed volume and the current freight rate market. Transit time is 20 to 30 days port-to-port, plus 5 to 7 days for customs clearance and delivery. Air freight from Shanghai to a major US airport costs approximately $2.50 to $5.00 per coat, depending on the coat's weight and the current air freight rate market. Transit time is 5 to 7 days door-to-door. The air freight premium is $2.00 to $4.00 per coat. For a brand placing a 500-unit order, the air freight premium totals $1,000 to $2,000. The decision to use air freight should be based on the value of speed. If the coats are needed for a specific launch event, a trade show, or a peak selling window that would be missed with ocean transit, the air freight premium is an investment in capturing full-price sales. A coat that sells for $89 at full margin generates approximately $58 in gross profit. The same coat sold at 40% off at end-of-season generates $27 in gross profit. The $31 difference in gross profit per unit far exceeds the $4 air freight premium. The air freight pays for itself through margin preservation. The key is to use air freight strategically for time-sensitive orders, not as a routine shipping method for planned production.

The Total Cost Model: From Factory Floor to Your Warehouse

The total cost model is the integration of the FOB cost and the hidden costs into a single, comprehensive figure that represents the true cost of placing a sellable coat in your warehouse. This figure is the foundation for your pricing strategy. Your wholesale price must cover the total landed cost plus your selling, general, and administrative expenses, plus your desired profit margin. Your retail price, if you sell direct-to-consumer, must cover the total landed cost plus your marketing, fulfillment, and overhead costs, plus your profit margin. A mistake in the total cost model is a mistake in the pricing strategy. The pricing strategy determines the brand's viability. The cost model is not an accounting detail. It is a strategic asset.

A complete total cost model for a women's summer coat includes the following line items, with representative values for a 500-unit order of a medium-complexity linen-blend trench coat imported from China to the US West Coast. FOB unit cost: $25.00. Ocean freight LCL per unit: $1.00. Marine insurance per unit: $0.13. US import duty at 27.7% of FOB: $6.93. Customs bond per unit: $0.15. Customs brokerage per unit: $0.40. Destination terminal handling per unit: $0.80. Drayage to warehouse per unit: $1.00. Total landed cost per unit: $35.41. This figure is the cost basis for all pricing decisions. If the brand sells wholesale at $52, the gross margin is $16.59, or 31.9%. If the brand sells direct-to-consumer at $89, the gross margin before marketing and fulfillment costs is $53.59, or 60.2%.

The total cost model should be built before the order is placed, not after the goods arrive. The FOB cost is obtained from the factory quotation. The freight rate is obtained from the freight forwarder or is included in the DDP quotation. The duty rate is verified from the HS code and the HTS lookup. The destination charges are estimated based on the port of entry and the shipment size. The cost model should include a contingency line of 2% to 3% of the total landed cost to cover unforeseen charges such as customs exams, port congestion surcharges, or fuel price increases. The contingency protects the margin from erosion by unpredictable events. The cost model is a living document. As actual invoices are received from the freight forwarder, the customs broker, and the trucking company, the estimated costs are replaced with actual costs. The comparison between estimated and actual costs provides feedback that improves the accuracy of future cost models.

How Should You Use the Cost Model to Set Wholesale and Retail Prices?

The cost model is the foundation of the pricing strategy. The pricing strategy has two components: the markup factor and the margin percentage. The markup factor is the multiple applied to the total landed cost to arrive at the selling price. A 2.5x markup on a landed cost of $35 gives a wholesale price of $87.50. The margin percentage is the portion of the selling price that is retained as gross profit. A wholesale price of $52 on a landed cost of $35 gives a gross margin of 32.7%. The appropriate markup or margin depends on the brand's distribution channel, competitive positioning, and cost structure. A wholesale brand selling to boutiques typically targets a 30% to 40% gross margin on the wholesale price. This requires a markup of 1.4x to 1.7x on the landed cost. A direct-to-consumer brand selling on its own website typically targets a 65% to 75% gross margin on the retail price. This requires a markup of 2.9x to 4.0x on the landed cost. The markup must also cover the brand's operating expenses: marketing, fulfillment, website hosting, photography, samples, travel, and salaries. A brand that fails to account for these expenses in its pricing model will generate gross profit but net loss. The cost model provides the floor. The pricing strategy builds the ceiling. The space between the floor and the ceiling is the brand's financial viability.

What Are the Most Common Costing Mistakes That Erode Margin?

I have observed five recurring costing mistakes that consistently erode brand margins. The first mistake is ignoring the duty rate. A brand owner uses the FOB cost plus a rough shipping estimate as the total cost, forgetting that import duties add 15% to 28% to the FOB value. The margin error is large and unavoidable once the goods arrive. The second mistake is underestimating the freight cost. The brand owner uses a spot rate quoted during a low-demand period and does not account for peak season surcharges, fuel surcharges, or currency adjustments. The actual freight cost is 30% to 50% higher than budgeted. The third mistake is not including the sample and development costs. The brand owner treats sampling as a one-time expense and does not amortize it across the production order quantity. For a small order of 200 units, sampling costs of $800 add $4.00 per unit to the true product cost. The fourth mistake is ignoring the payment processing fees. Trade Assurance, PayPal, and credit card fees add 3% to 5% to the order value. A $20,000 order incurs $600 to $1,000 in payment processing costs. The fifth mistake is not building a contingency for quality issues. A 2% defect rate on a 500-unit order means 10 unsellable coats. The cost of those 10 coats, including their share of freight and duty, is borne by the 490 sellable coats, reducing the margin on every unit sold. The prevention for all five mistakes is the same: build a complete, line-by-line cost model with realistic, verified inputs and a contingency allowance. The model takes one hour to build and can save tens of thousands of dollars in margin erosion.

Conclusion

The true cost of manufacturing a women's summer coat is a structured, knowable figure composed of seven cost categories spanning the journey from fabric mill to your warehouse. The FOB cost, covering fabric, trims, labor, and factory margin, represents approximately 60% to 70% of the total landed cost. The hidden costs, freight, duty, brokerage, and destination charges, represent the remaining 30% to 40%. The total landed cost for a quality summer coat from a compliant Chinese factory, shipped to a US warehouse, ranges from $22 to $35 per unit for typical designs and order quantities.

The brand owner who understands this cost structure has a significant competitive advantage. They can negotiate with factories from a position of knowledge, not optimism. They can evaluate fabric options with a clear view of the cost impact. They can choose shipping modes with a precise understanding of the speed-versus-cost trade-off. They can set wholesale and retail prices that are competitive yet profitable. They can build a business that survives beyond the first production run.

At Shanghai Fumao, transparency is a core operating principle. We provide detailed FOB cost breakdowns to every prospective brand partner. We provide accurate HS codes and estimated duty rates. We provide DDP quotations that bundle all hidden costs into a single, predictable per-unit price. We want our brand partners to know their costs because a partner who knows their costs is a partner who prices profitably, grows sustainably, and stays in business. Short-term relationships are built on information asymmetry. Long-term partnerships are built on shared knowledge.

If you are developing a summer coat collection and want a transparent cost breakdown for your specific designs, contact our Business Director, Elaine. Provide your design sketches or tech packs, your target fabric and order quantity. She will return a detailed cost sheet with FOB cost components, estimated duty, freight, and destination charges, and a total landed cost per unit. You can build your pricing model on real numbers, not guesses. Email Elaine at: elaine@fumaoclothing.com.