About six years ago, I received a desperate phone call from a brand owner who had just lost $40,000. He had found a factory on a sourcing platform, negotiated what he thought was a great FOB price for 5,000 pairs of classic chino shorts, and wired a 50% deposit to start production. The factory sent him a few photos of fabric rolls and a cutting table. Then the communication slowed. Then it stopped. The factory stopped responding to emails and phone calls. The deposit was gone. There was no product, no refund, and no practical legal recourse. He had made a single, catastrophic mistake. He had sent a large deposit to an unverified factory with no payment protection, no inspection contingency, and no leverage. I told him that the payment terms, more than the quality spec, more than the price, should have been the most heavily negotiated part of his contract.

The payment terms that protect a buyer ordering classic shorts from abroad are structured around the principle of aligning payment milestones with verifiable production progress, with the standard protective structure being a 30% deposit to initiate production, a 30% payment against photographic or video evidence of the completed bulk production, and the 40% balance against a passed third-party pre-shipment inspection report or against the bill of lading, while avoiding at all costs a 50% or higher upfront deposit, a payment in full before shipment, or any payment method that does not offer a dispute resolution mechanism such as a wire transfer to an unverified account.

At Shanghai Fumao, I have been on both sides of the payment negotiation. I understand the factory's need for security, and I understand the buyer's need for protection. The goal of good payment terms is not to disadvantage the factory. It is to create a structure where both parties are protected, where neither party is bearing disproportionate risk, and where the incentives are aligned toward a successful, on-time, on-quality delivery. Let me walk you through exactly how to structure those terms.

What Payment Structure Aligns Incentives for Both Buyer and Factory?

The payment structure is not just a schedule of cash flows. It is the primary mechanism for aligning the factory's incentives with the buyer's interests. A factory that has been paid in full before production begins has no financial incentive to prioritize the buyer's order, to maintain quality, or to deliver on time. The buyer has already paid. The factory's incentive is to serve the next client, the one whose payment is still contingent on performance. A well-structured payment schedule keeps the factory financially motivated to perform at every stage of the process.

A payment structure that aligns incentives protects the buyer by tying each payment to a specific, verifiable milestone that demonstrates the factory's progress and commitment, provides the factory with sufficient working capital to purchase raw materials and fund production without requiring the factory to finance the entire order from its own reserves, and reserves a significant final payment, typically 30% to 40%, until the goods have passed an independent quality inspection, creating a powerful financial incentive for the factory to meet the agreed quality standards and delivery timeline.

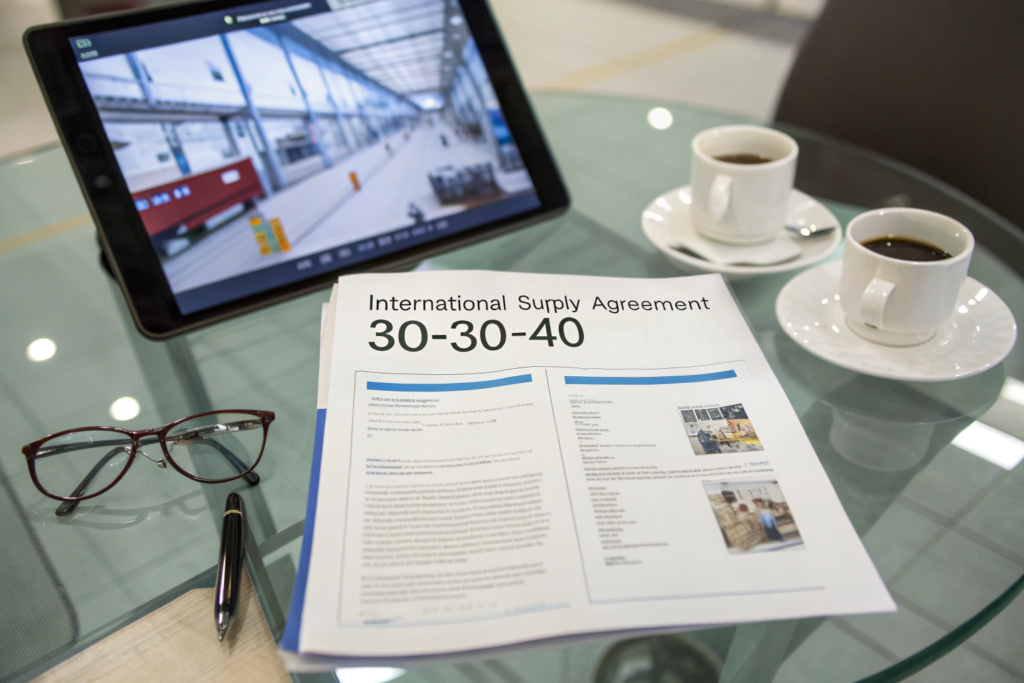

Why Is the 30-30-40 Structure the Industry Standard for Protective Terms?

The 30-30-40 structure is the most commonly used protective payment schedule in international apparel sourcing. The 30% deposit is paid upon order confirmation. This payment covers the factory's raw material cost. The factory can purchase the fabric and trims without financing the purchase from its own working capital. The deposit is the buyer's commitment to the order.

The second 30% is paid upon evidence of completed production. The factory provides photographs or, preferably, a live video walkthrough of the finished, packed goods. The buyer verifies that the goods exist, that they are labeled and packed, and that the quantity is correct. The payment is released. The factory now has 60% of the total order value. The remaining 40% balance is paid against a passed third-party pre-shipment inspection report. The inspector has examined a random sample, confirmed that the quality meets the AQL standard, and issued a pass report. The buyer releases the final payment. The factory ships the goods. This structure balances the factory's need for working capital with the buyer's need for quality assurance and delivery security. This international trade payment terms framework is the foundation of a secure sourcing relationship.

When Can a Letter of Credit Provide Additional Protection?

A Letter of Credit is a bank-issued guarantee of payment. The buyer's bank issues the LC, which states that the bank will pay the factory upon presentation of specific, pre-agreed documents, typically the bill of lading, the commercial invoice, the packing list, and a certificate of inspection. The LC removes the payment risk from the buyer-factory relationship and places it with the banks.

For a first-time relationship, or for a very large order, an LC provides a level of protection that open account terms cannot match. The factory knows that the payment is guaranteed by the buyer's bank, so the factory is willing to produce the order without a large upfront deposit. The buyer knows that the payment will not be released until the factory presents the required documents, including the inspection certificate if specified. The LC is more complex and more expensive than open account terms, involving bank fees and documentation requirements. It is typically used for orders above $50,000 or for initial orders with a new factory. This letter of credit for international trade mechanism is the gold standard for payment security, but it is not necessary or cost-effective for every transaction.

What Specific Milestones Should Trigger Payment Releases?

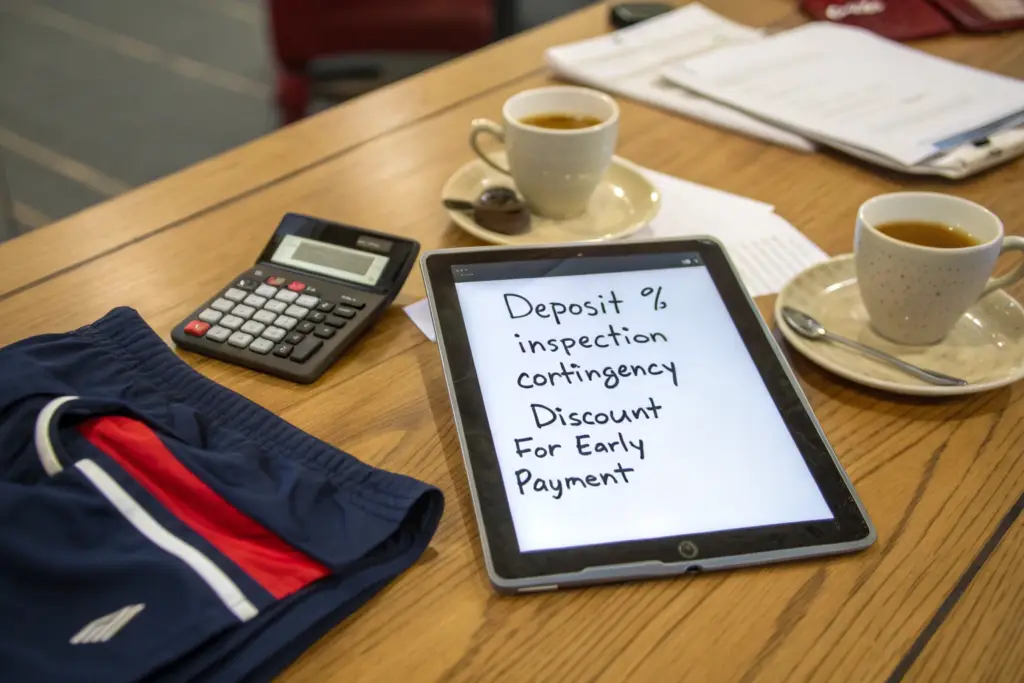

Vague milestones create disputes. "30% upon production start" is vague. The buyer and the factory may have different definitions of when production has started. The factory considers production started when the fabric is ordered. The buyer considers production started when the cutting begins. The ambiguity creates conflict. Specific, verifiable milestones eliminate the conflict. The milestone is either objectively met or it is not. There is no gray area to argue over.

Each payment milestone in a classic shorts purchase order should be tied to a specific, objectively verifiable event that is documented with evidence, with the initial deposit triggered by the mutual execution of the purchase order and the receipt of a proforma invoice, the progress payment triggered by photographic or video evidence of the completed bulk production with the goods identifiable by the buyer's brand labels and packaging, and the final balance triggered by a passed third-party pre-shipment inspection report or, if no third-party inspection is used, by the presentation of the bill of lading proving the goods have been loaded onto the vessel.

What Constitutes Acceptable Evidence of Completed Production?

The progress payment is the most vulnerable point in the payment schedule. The buyer is sending a significant amount of money based on evidence that the goods exist. If the evidence is fabricated or misleading, the buyer is paying for goods that do not exist or are not theirs.

The evidence must be specific and current. The factory should provide photographs or video of the finished, packed cartons. The cartons should be clearly marked with the buyer's shipping marks, the purchase order number, the destination, and the carton numbers. The video should show a wide shot of the full shipment, then zoom in on individual cartons to show the markings, then open a carton to show the contents. The buyer should compare the carton markings and the contents against the packing list. This verification takes minutes and can prevent a catastrophic loss. This production verification before payment step is non-negotiable for a protective payment process.

How Does a Third-Party Inspection Report Function as a Payment Trigger?

The third-party inspection is the buyer's independent quality verification. An inspector from a firm like SGS, Bureau Veritas, or Intertek visits the factory, draws a random sample from the finished, packed cartons, and inspects the shorts against the buyer's specifications and the agreed AQL standard.

If the inspection passes, the inspector issues a pass report. The buyer releases the final payment. The factory ships the goods. If the inspection fails, the buyer does not release the payment. The factory must rework the defective goods and submit to a re-inspection. The payment is held until the inspection passes. This mechanism gives the buyer enormous leverage over quality. The factory knows that the final 40% of the order value is contingent on the shorts meeting the standard. The financial incentive to get the quality right is direct and powerful. This third-party inspection as payment condition is the strongest quality protection available to an international buyer.

What Payment Methods Offer Recourse If Something Goes Wrong?

The method of payment is as important as the timing of payment. A wire transfer, once sent, is gone. The money has left the buyer's account and is in the factory's account. The buyer's ability to recover the funds in the event of non-delivery, fraud, or a major quality dispute is extremely limited. Other payment methods, while more expensive or less convenient, offer recourse mechanisms that can protect the buyer. The choice of payment method is a risk management decision.

Payment methods that offer buyer protection for international classic shorts orders include credit cards, which provide chargeback rights under the card network's rules for non-delivery or goods significantly not as described; PayPal, which offers a dispute resolution process for eligible transactions; and Letters of Credit, which guarantee payment only against compliant documents and can be structured to require an inspection certificate, while wire transfers, the most common method, offer no inherent recourse and should only be used with verified, trusted factories under a protective milestone-based payment structure.

What Protections Do Credit Cards and PayPal Offer for Sourcing Transactions?

Paying a factory by credit card is not always possible. Many factories, particularly smaller ones, do not accept credit cards. But when it is possible, it provides significant protection. The card networks, Visa, Mastercard, and American Express, have chargeback rules that allow the buyer to dispute a transaction and recover funds if the goods are not delivered, or if the goods delivered are significantly not as described. The burden of proof is on the merchant, the factory, to demonstrate that the goods were delivered as agreed.

PayPal offers a similar dispute resolution process for eligible transactions. The buyer opens a dispute, provides evidence of the problem, and PayPal adjudicates. The process is not perfect, it can be slow, and the outcome is not guaranteed, but it provides a path to recovery that a wire transfer does not. The primary limitation is that these methods typically involve transaction fees of 3% to 5%, which the factory or the buyer must absorb. This secure payment methods for international sourcing trade-off between cost and protection should be evaluated for each transaction.

Why Is a Wire Transfer to an Unverified Account the Riskiest Option?

A wire transfer to an unverified account is the payment equivalent of handing cash to a stranger. The money moves instantly, irrevocably, and across international borders. The buyer's bank cannot reverse the transaction. The factory's bank is under no obligation to assist. Law enforcement in either country is unlikely to pursue a commercial dispute of the size typical for a classic shorts order.

The only protection against wire transfer fraud is verification before the transfer. The buyer must verify that the factory exists, that the bank account belongs to the factory, and that the factory's legal entity name matches the name on the bank account. The buyer should conduct a video tour of the factory, verify the business license, and check the factory's references. The first payment to a new factory should be as small as possible, perhaps a sample development fee, to test the payment channel and the factory's responsiveness before committing to a large deposit. This wire transfer fraud prevention in international trade due diligence is the essential precondition for using wire transfers safely.

How Can a Buyer Negotiate Better Terms with a Factory?

Payment terms are negotiable. A factory's initial proposal is its preferred position, not its final position. A buyer who accepts the initial terms without negotiation is leaving protection on the table. A buyer who negotiates aggressively and unreasonably may damage the relationship before it begins. The goal is to negotiate terms that protect the buyer without making the factory feel that it is bearing all the risk.

A buyer can negotiate better payment terms with a shorts factory by offering value in exchange for protection, such as accepting a slightly higher FOB price in return for a lower deposit percentage, committing to a larger order volume or a multi-order program in return for more favorable payment milestones, providing the factory with prompt payment upon milestone completion to build a track record of reliability that makes the factory more willing to accept protective terms on future orders, and framing the negotiation as a mutual risk management exercise rather than a zero-sum demand, emphasizing that the protective terms are standard industry practice and are in place to protect the long-term partnership, not to express distrust.

What Tradeables Can a Buyer Offer to Secure a Lower Deposit?

A factory that asks for a 50% deposit is often trying to cover the raw material cost plus some labor cost. The factory may be financially constrained, or it may have been burned by a previous client who did not pay the balance. The buyer who wants to reduce the deposit must address the factory's underlying concern.

The buyer can offer to pay for the fabric and trims directly, with the factory providing the supplier invoices. The buyer pays the fabric mill and the trim supplier directly. The factory has no raw material cost exposure. The deposit can be reduced to 10% or eliminated entirely. The buyer can offer to provide a letter of credit instead of a deposit. The factory's bank will confirm the LC, and the factory knows the payment is guaranteed. The buyer can offer a shorter payment cycle. Instead of a 30-30-40 structure, the buyer can offer 30% deposit and 70% against the bill of lading, with no progress payment. The factory receives a larger share of the payment earlier. This negotiating payment terms with suppliers trade-based approach addresses the factory's needs while achieving the buyer's protection goals.

How Should the Negotiation Be Framed to Preserve the Relationship?

A payment term negotiation that feels adversarial damages the relationship before the first order is placed. The factory feels that the buyer does not trust it. The buyer feels that the factory is being unreasonable. The partnership begins with suspicion.

The negotiation should be framed as a collaborative risk management exercise. The buyer explains that the proposed terms are standard for the industry, are required by the buyer's investors or board, and are designed to protect both parties. The buyer emphasizes that the first order is the beginning of a long-term relationship, and that as the relationship matures and trust is built, the terms can evolve. The factory that understands that the protective terms are not personal, but professional, is more likely to accept them. This supplier negotiation relationship management approach builds the foundation for a long-term partnership.

Conclusion

The payment terms that protect a buyer ordering classic shorts from abroad are not a technical detail buried in the purchase order. They are the most important risk management tool the buyer has. A well-structured payment schedule, typically a 30-30-40 split tied to order confirmation, production completion verification, and passed inspection, aligns the factory's financial incentives with the buyer's quality and delivery goals. A payment method that offers recourse, a credit card, PayPal, or a letter of credit, provides a path to recovery if something goes wrong. A negotiation strategy that offers value in exchange for protection preserves the relationship while achieving the buyer's security requirements.

The buyer who treats payment terms as a secondary concern, who wires a 50% deposit to an unverified account without a signed contract, without inspection contingencies, and without verification milestones, is not buying shorts. They are buying a lottery ticket. Sometimes they win. Sometimes they lose $40,000.

At Shanghai Fumao, we work with our brand partners to establish payment terms that are fair, transparent, and protective for both sides. We understand that a buyer who feels secure is a buyer who will grow with us over the long term. If you are developing a classic shorts program and want to ensure your payment terms are structured for protection, contact our Business Director, Elaine, at elaine@fumaoclothing.com. Let's build a payment structure that lets you sleep at night.