Eighteen months ago, I sat down with a brand owner who had made a decision that was costing him money. He had shifted his entire classic shorts production from China to Vietnam two years earlier, convinced that he was escaping the Section 301 tariffs and reducing his costs. He had not done the full landed cost math. He had compared the FOB prices, saw that Vietnam was slightly higher, and assumed the tariff savings would more than compensate. When we finally built a complete cost model together, accounting for the higher fabric costs in Vietnam, the longer transit times, the higher financing costs, and the additional quality control travel, the Vietnam product was actually 8% more expensive than the China product on a landed, duty-paid basis. He had been losing margin for two years without realizing it.

Comparing the real cost per unit for classic shorts from China versus Vietnam requires building a complete landed cost model that goes far beyond the FOB price quoted by each factory, incorporating the baseline HTS import duty, any additional punitive tariffs such as the Section 301 duties on Chinese goods, the ocean freight differential based on transit distance and port congestion, the inventory carrying cost of goods tied up in longer transit times, the per-unit allocation of quality control and compliance travel, and the often-overlooked cost of development, sampling, and communication inefficiency, with the total revealing that China often remains cost-competitive despite the tariff headwind due to its deeper, more efficient supply chain.

At Shanghai Fumao, I have helped numerous brand partners evaluate the true cost of their sourcing decisions. The comparison between China and Vietnam is the most common analysis I perform. The answer is never obvious, and the wrong assumption is always expensive. Let me walk you through every cost element that belongs in the model, and show you how to build a comparison that reflects the real economics of your specific product.

What Are the Real FOB Cost Components Beyond the Unit Price?

The FOB price, the cost of the goods loaded onto the vessel at the port of origin, is the starting point of any comparison. But the FOB price itself is a composite of multiple underlying cost factors, and those factors differ systematically between China and Vietnam. A buyer who treats the FOB price as a single number to be compared directly is missing the structural differences that determine whether the price is sustainable, negotiable, or likely to increase.

The real FOB cost of classic shorts from any country is composed of four primary elements: fabric cost, which typically accounts for 50% to 60% of the total and is significantly influenced by whether the country has a domestic textile industry capable of producing the required fabric or must import it from China or elsewhere, trim and component cost, which includes zippers, buttons, interlining, labels, and packaging and is similarly dependent on domestic supply chain depth, direct labor cost, which is the sewing operator time multiplied by the prevailing wage rate, and factory overhead and margin, which reflects the cost of utilities, facilities, compliance, and the factory's required profit, with China generally maintaining an advantage in fabric and trim cost due to its vertically integrated textile industry, while Vietnam offers a labor cost advantage that is offset by higher material import costs.

How Does China's Vertical Textile Integration Lower Fabric Costs?

China possesses the world's most complete textile manufacturing ecosystem. Cotton is grown domestically. Yarn is spun domestically. Fabric is woven, dyed, and finished domestically. Trim components, zippers, buttons, interlinings, thread, labels, and packaging, are manufactured domestically. A factory in Shanghai or Guangdong can source every component of a pair of classic shorts within a few hundred kilometers.

This vertical integration eliminates multiple layers of freight, import duty, and intermediary margin that are baked into the fabric cost in countries with less developed textile industries. Vietnam has a strong and growing garment manufacturing sector, but its textile industry is less developed. A significant percentage of the fabric used in Vietnamese garment factories is imported from China. The fabric travels from a Chinese mill to a Vietnamese port, incurs Vietnamese import duty, and is trucked to the Vietnamese factory. Each of those steps adds cost. The fabric that a Chinese factory buys for $3.50 per meter might cost a Vietnamese factory $4.20 per meter for the identical cloth. This fabric cost differential, multiplied across the 1.2 to 1.5 meters required for a pair of classic shorts, can add $0.85 to $1.05 to the FOB cost per unit in Vietnam. This textile supply chain China vs Vietnam structural difference is the single largest factor in the FOB comparison.

How Do Labor Cost and Productivity Differ Between the Two Countries?

Vietnam's garment worker wages are lower than those in China's coastal manufacturing regions. The average hourly labor cost for a sewing operator in Vietnam is approximately 40% to 50% lower than in Shanghai or Guangdong. This labor cost advantage is real and significant.

However, labor cost is not the same as labor cost per unit. The labor cost per unit is the hourly wage multiplied by the time required to produce the unit. Productivity, the number of units produced per operator per hour, matters as much as the wage rate. Chinese factories have generally invested more heavily in automation, lean manufacturing, and workforce training. A Chinese operator using a modern, well-maintained machine with optimized workstation layout may produce 15% to 25% more units per hour than a Vietnamese operator in a less developed factory. The productivity gap partially offsets the wage gap. Additionally, China's workforce includes a larger pool of experienced operators who have spent decades in the industry and can efficiently produce complex, high-quality garments. This garment manufacturing labor cost comparison nuance is why comparing wage rates alone produces a misleading result.

How Do Tariffs and Duties Change the Landed Cost Equation?

The FOB price comparison tells you what you pay the factory. The landed cost comparison tells you what you pay to have the goods in your warehouse, ready to sell. The largest single difference between the FOB price and the landed cost is the import duty and tariff burden. This is the factor that initially drives many buyers to consider Vietnam, and it is the factor that is most frequently misunderstood or oversimplified in sourcing decisions.

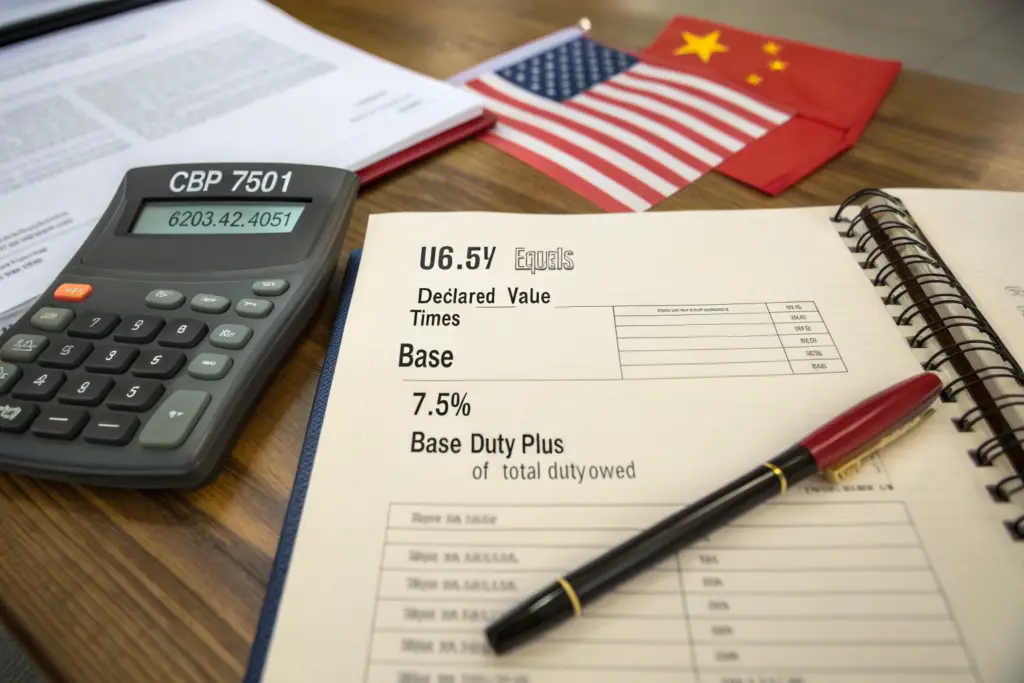

The duty and tariff differential between China and Vietnam for classic shorts imports is substantial, with Chinese-origin shorts currently subject to the baseline HTS duty of 16.5% for woven cotton shorts plus an additional Section 301 tariff of 7.5%, for a total duty burden of 24% of the declared value, while Vietnamese-origin shorts are subject only to the baseline HTS duty of 16.5%, creating a 7.5 percentage point duty advantage for Vietnam that must be weighed against the FOB cost differential and other landed cost factors.

What Is the Exact Duty Calculation for a Classic Short from Each Country?

The duty calculation follows a specific sequence. The baseline HTS duty is calculated first. For a woven cotton men's short, HTS 6203.42.4051, the rate is 16.5%. The duty is 16.5% of the entered value, which is the FOB price paid to the factory.

For a Chinese-origin short, the Section 301 tariff is calculated on top of the baseline duty. The current List 3 rate is 7.5%. This 7.5% is applied to the entered value, not to the value plus baseline duty. For a short with a $10.00 FOB price, the baseline duty is $1.65. The Section 301 duty is $0.75. The total duty is $2.40, which is 24% of the FOB price. For a Vietnamese-origin short with the same $10.00 FOB price, the baseline duty is $1.65. There is no Section 301 duty. The total duty is $1.65, which is 16.5% of the FOB price. The duty differential is $0.75 per unit in this example. This import duty calculation apparel is the math that drives many sourcing decisions. The key question is whether the FOB price in Vietnam is more than $0.75 higher than the FOB price in China. If it is, as it often is due to fabric import costs, the duty advantage is negated.

How Might Section 301 Changes Affect the Future Comparison?

The Section 301 tariffs are currently under a statutory four-year review. They could increase, decrease, or be terminated. They could be modified through exclusions that apply to specific product categories. A brand making a multi-year sourcing commitment needs to consider not just the current tariff differential but the range of possible future differentials.

A termination of Section 301 tariffs on Chinese apparel would eliminate Vietnam's duty advantage entirely. The comparison would revert to a pure FOB and logistics comparison, which China would likely win on most classic shorts programs due to its supply chain efficiency. An increase in Section 301 tariffs, back to the original 25% rate that was in effect for List 3 goods at one point, would swing the pendulum significantly in Vietnam's favor, adding roughly $2.50 per unit in additional duty cost to Chinese shorts relative to Vietnamese shorts. This tariff policy scenarios uncertainty is a risk factor that must be incorporated into sourcing strategy. A brand that diversifies its sourcing across both countries is hedging this policy risk.

What Logistics and Inventory Costs Differ Between China and Vietnam?

The moment the factory finishes producing the shorts and hands them to the freight forwarder, the clock starts on a series of costs that are not captured in the FOB price. These logistics and inventory costs accumulate every day the goods are in transit, and the accumulation period is systematically longer for some countries than for others. A comparison that ignores these costs is missing a significant component of the true cost per unit.

The logistics and inventory cost differential between China and Vietnam for classic shorts includes measurable differences in ocean freight transit time, with China-to-US West Coast typically requiring twelve to sixteen days and Vietnam-to-US West Coast typically requiring eighteen to twenty-five days due to less frequent direct sailings and more common transshipment through regional hub ports, in freight rates, which are currently higher for Vietnamese ports due to lower container volume and less carrier competition, and in inventory carrying cost, which accrues on the value of the goods for every additional day they are in transit, representing a real financing cost that must be allocated to each unit.

How Do Transit Times and Freight Rates Compare Between the Two Origins?

The distance from Shanghai to Los Angeles is approximately 5,700 nautical miles. The distance from Ho Chi Minh City to Los Angeles is approximately 7,200 nautical miles, a difference of about 25%. The direct transit time reflects this distance difference, but the practical difference is often larger due to service frequency and routing.

Shanghai and Ningbo are among the busiest container ports in the world, with daily direct sailings to major US West Coast ports. A container of classic shorts from Shanghai to Los Angeles can be on a direct vessel within days of being ready. Ho Chi Minh City has fewer direct sailings. Containers are frequently transshipped through Singapore, Hong Kong, or other hub ports, adding days of transit time and increasing the risk of missed connections. The total door-to-door transit time from a Chinese factory to a US warehouse is typically thirty to thirty-five days. From a Vietnamese factory, it is often forty to fifty days. The freight rate per container is currently higher from Vietnam due to lower volume and less carrier competition. This ocean freight transit times Asia to US differential adds both direct freight cost and time-related inventory cost.

What Is the Inventory Carrying Cost of Longer Transit Times?

Every day that a pair of shorts is in transit is a day that the capital used to pay for those shorts is unavailable for other purposes. The cost of that tied-up capital is the inventory carrying cost, and it is a real, calculable expense.

The inventory carrying cost per unit is calculated by taking the FOB cost of the unit, multiplying it by the brand's cost of capital, typically 8% to 15% annually for a small to mid-size brand, and prorating that annual cost over the number of days the goods are in transit. A pair of shorts with a $10.00 FOB cost and a brand cost of capital of 12% incurs approximately $0.0033 per day in financing cost. Over a thirty-five-day China transit, the carrying cost is approximately $0.12 per unit. Over a forty-five-day Vietnam transit, it is approximately $0.15 per unit. The difference is $0.03 per unit, which is small but real and adds to the other Vietnam cost premiums. The more significant carrying cost is the cost of the additional safety stock that a brand must hold to compensate for the longer and more variable transit time. This inventory carrying cost calculation can add a more substantial per-unit allocation.

What Hidden Quality and Management Costs Affect the Total Comparison?

Some of the most significant costs in international sourcing never appear on a factory invoice or a freight forwarder's bill. They are the management costs, the travel costs, the communication costs, and the quality failure costs that the brand incurs to manage the supplier relationship. These costs are real, they are variable by country, and they can be substantial enough to swing the total cost comparison. Ignoring them because they are hard to quantify does not make them disappear. It just makes the cost comparison inaccurate.

The hidden quality and management costs that differ between China and Vietnam include the travel and accommodation expense for factory visits, audits, and inline quality inspections, which are typically higher and more frequent for a less mature production relationship, the communication and development efficiency cost reflecting the number of sample rounds, the clarity of technical communication, and the speed of problem resolution, and the quality failure and rework cost, which accounts for the financial impact of defects that must be corrected or that reach the customer, with each of these costs being influenced by the maturity and experience of the factory base in each country.

How Do Supplier Development and Communication Efficiency Compare?

China has been manufacturing apparel for export markets for over thirty years. The factory base includes thousands of facilities with deep experience producing for American and European brands. Factory management understands Western quality expectations, communication norms, and business practices. The learning curve for a new brand relationship is relatively short.

Vietnam's apparel export industry is younger. There are excellent factories in Vietnam, but the base of experienced, export-ready factories is smaller. A brand may need to invest more time and resources in supplier identification, factory auditing, and quality system development. Communication may require more translation support. The sample development process may involve more iterations because the factory is less familiar with the specific requirements of the US market. These inefficiencies have a cost. The brand is spending management time, and management time is a scarce and expensive resource. This supplier development and management cost is difficult to quantify precisely but should be estimated and included in the comparison as a reasonable allocation per unit.

How Should Quality Failure and Rework Costs Be Modeled?

Every sourcing relationship has a defect rate. The question is not whether defects occur, but at what rate, and what the consequences of those defects cost. The cost of quality is the cost of preventing defects, plus the cost of detecting defects, plus the cost of correcting defects that escape detection. The cost of correcting defects in the destination country is many times higher than the cost of correcting them at the factory.

If a Chinese factory with a mature quality system produces shorts with a major defect rate of 2% and a Vietnamese factory with a less developed system produces shorts with a major defect rate of 5%, the 3 percentage point difference in defect rate has a direct financial cost. The cost includes the freight for returned goods, the inspection labor to identify the defects, the rework cost or the write-off cost for unsaleable units, and the lost margin on units that cannot be sold. This cost should be estimated based on the factory's audit results, references, and historical performance, and included in the total cost model. This cost of quality in sourcing principle applies regardless of the country of origin but is influenced by the maturity of the factory base. At Shanghai Fumao, we maintain a defect rate below 1% through our integrated quality systems, and we provide the data to support our partners' cost modeling.

Conclusion

Comparing the real cost per unit for classic shorts from China versus Vietnam requires a discipline that many sourcing decisions lack. The comparison cannot stop at the FOB price, which is misleading on its own. It cannot stop at the FOB price plus the tariff differential, which is the most common shortcut and the most common source of error. It must extend to every cost that is incurred between the factory floor and the customer's hands.

The complete model includes the fabric and trim cost advantage that China's integrated supply chain provides, which often offsets Vietnam's labor cost advantage. It includes the duty and tariff burden, where Vietnam currently has a clear advantage that is subject to policy change. It includes the logistics cost differential, the freight, the transit time, and the inventory carrying cost, where China's shorter, more frequent sailings provide a consistent advantage. It includes the hidden management costs, the travel, the communication, and the quality failure expense, where China's mature factory base provides an efficiency advantage that is real but hard to quantify.

When all of these costs are included, the comparison often reveals that China remains cost-competitive for many classic shorts programs despite the Section 301 tariff headwind, particularly for products that use fabrics and trims from China's domestic supply chain, that require complex construction, or that are produced in moderate volumes. Vietnam offers a compelling alternative for simpler products, higher volumes, and brands willing to invest in supplier development. The optimal strategy for many brands is not to choose one country over the other, but to maintain qualified factory relationships in both, allocating production based on the specific product, the specific timeline, and the specific cost model at the time of order.

At Shanghai Fumao, we help our brand partners build accurate total cost models for their specific products. We provide transparent FOB cost breakdowns, logistics cost estimates, and quality performance data. If you are comparing sourcing options for your classic shorts program, contact our Business Director, Elaine, at elaine@fumaoclothing.com. Let's build the model that tells you the real cost, not just the factory price.