I sat in a coffee shop in Los Angeles last year with a buyer who ran a chain of eight boutiques. She was one of the most successful multi-brand retailers I knew. I asked her what her secret weapon was. I expected her to talk about visual merchandising or social media marketing. Instead, she leaned forward and said two words: "Payment terms." She explained that she refuses to work with brands that demand 100% payment upfront. She negotiates Net 60 terms on every order she places. That means she receives the goods, puts them on her sales floor, and often sells through 40% of the inventory before a single dollar leaves her bank account. Her cash flow is not a constraint on her buying decisions. It is a strategic asset that allows her to take risks on new brands, place larger orders on proven sellers, and sleep soundly knowing she is not gambling her rent money on a shipment that might arrive late.

Highly flexible payment terms are a massive strategic advantage for busy apparel buyers because they solve the fundamental cash flow timing problem that kills small retailers. In the standard model, the buyer pays the supplier 30 to 90 days before the goods arrive, then waits another 30 to 60 days to sell through the inventory. Their cash is trapped in transit and on shelves for up to five months. Flexible terms, such as a low 20-30% deposit with the balance due Net 30 or Net 60 after shipment, flip this timeline. The buyer pays the majority of the invoice after the goods have already arrived and begun selling. This allows them to partially self-fund the inventory through sales, reduces their reliance on expensive short-term loans or credit cards, and frees up working capital to invest in marketing, store experience, or larger buys from their best-selling brands. It is not just a convenience. It is a cash flow arbitrage that makes the difference between a store that survives a slow season and one that closes its doors.

Flexible payment terms are not a favor the factory does for the buyer. They are a strategic partnership tool that aligns incentives. When a buyer pays upfront, the factory has the cash, and the risk shifts entirely to the buyer. When a buyer pays after delivery, both parties share the risk and the reward. The factory is incentivized to deliver quality goods on time because their payment depends on the buyer’s satisfaction. I want to share exactly how flexible payment structures work, why they benefit both the buyer and the manufacturer, and how you can negotiate them into your own purchasing agreements.

How Do Flexible Deposit Structures Free Up Working Capital for Multi-Brand Boutique Buyers?

A buyer I know runs a highly curated boutique in Austin, Texas. She has a $30,000 open-to-buy budget for the autumn season. If she pays 100% upfront, she can only afford to stock about $30,000 worth of inventory, and she has to guess correctly on every single style because she has no buffer. If a style bombs, her money is gone. Two years ago, she shifted to working exclusively with brands that accepted a 30% deposit with the balance due Net 45. Her same $30,000 cash outlay now allowed her to place $85,000 worth of orders because she only needed to cover the deposits upfront. The balance would be due after the goods had already been selling for two weeks. Her revenue that season jumped 40%. Her risk per style dropped dramatically because she could spread her bets across a wider assortment. The flexible deposit structure turned her from a cautious, understocked buyer into a confident, fully stocked merchant.

A flexible deposit structure, typically 20% to 30% upfront with the balance due 30 to 60 days after shipment, is the single most effective cash flow tool for a multi-brand boutique buyer. It reduces the initial cash outlay by 70% to 80%, allowing the buyer to place orders with multiple brands simultaneously rather than choosing between them. This means a deeper, more interesting assortment for the end consumer. It also creates a natural quality assurance mechanism. If the goods arrive damaged or not as specified, the buyer has significant leverage to negotiate a remedy because the majority of the payment is still in their control. This structure converts the buyer-supplier relationship from a cash-and-carry transaction into a credit-based partnership built on mutual trust and performance. The buyer gains the financial bandwidth to operate like a much larger retailer.

The deposit is the key lever. A factory that asks for 50% or 100% upfront is essentially asking the buyer to finance the entire production run and bear all the risk of non-delivery. A factory that accepts a 20% to 30% deposit is putting its own skin in the game. The deposit covers the raw material cost, so the factory’s risk is limited. The balance incentivizes the factory to deliver exactly what the buyer ordered.

How Can a 30/70 Payment Structure Allow a Boutique to Open Three Times More Brands Per Season?

The math is simple and powerful. A boutique has $20,000 in cash for season open-to-buy. With 100% upfront terms, the buyer can place $20,000 in total orders, perhaps from four brands at $5,000 each. With a 30% deposit and Net 60 balance, the same $20,000 cash outlay can fund $66,000 in total orders because only $20,000 is needed for the deposits. The buyer can now work with 12 brands instead of four. This transforms the store’s assortment from predictable and safe to diverse and exciting. The customer walks in and sees fresh labels they have never seen before. The store becomes a destination for discovery. The working capital management strategies for retailers are built on exactly this principle. Cash should be deployed to maximize assortment depth, not tied up in transit.

Why Does Deferred Payment Act as a Natural Insurance Policy Against Late or Defective Shipments?

When a buyer has paid 100% upfront, and the shipment arrives two weeks late with defective units, the buyer has no leverage. They can beg for a discount. They can threaten to never order again. But the factory already has all the money. The factory’s incentive to resolve the problem quickly is weak. When the buyer has only paid a 30% deposit, the dynamic reverses. The buyer still holds 70% of the payment. They can say, "I will release the balance payment once you ship the replacement units for the defects." Or, "We need to discuss a discount for the late delivery before I process the final payment." The deferred balance is the buyer’s insurance policy. It ensures the factory remains responsive and accountable until the goods are on the sales floor and generating revenue. We see this dynamic play out constantly. The factories that accept deferred payment are the factories that are confident in their quality and delivery. The factories that demand 100% upfront are often the ones that expect problems.

What Are the Specific Payment Term Structures That Top-Tier Chinese Manufacturers Actually Offer?

A brand owner once told me he assumed all Chinese factories demanded 100% upfront. That was his experience with the trading companies he found on Alibaba. He believed it was an industry standard. He was shocked when I explained our standard terms: 30% deposit to secure the production slot and purchase raw materials, and the 70% balance paid after the goods pass final inspection and before shipment. This is called "TT against inspection." It is the norm among established, financially stable factories. The factories that demand 100% upfront are often undercapitalized trading companies that need your deposit to pay for the last client’s order. They are not manufacturers. They are cash-flow intermediaries.

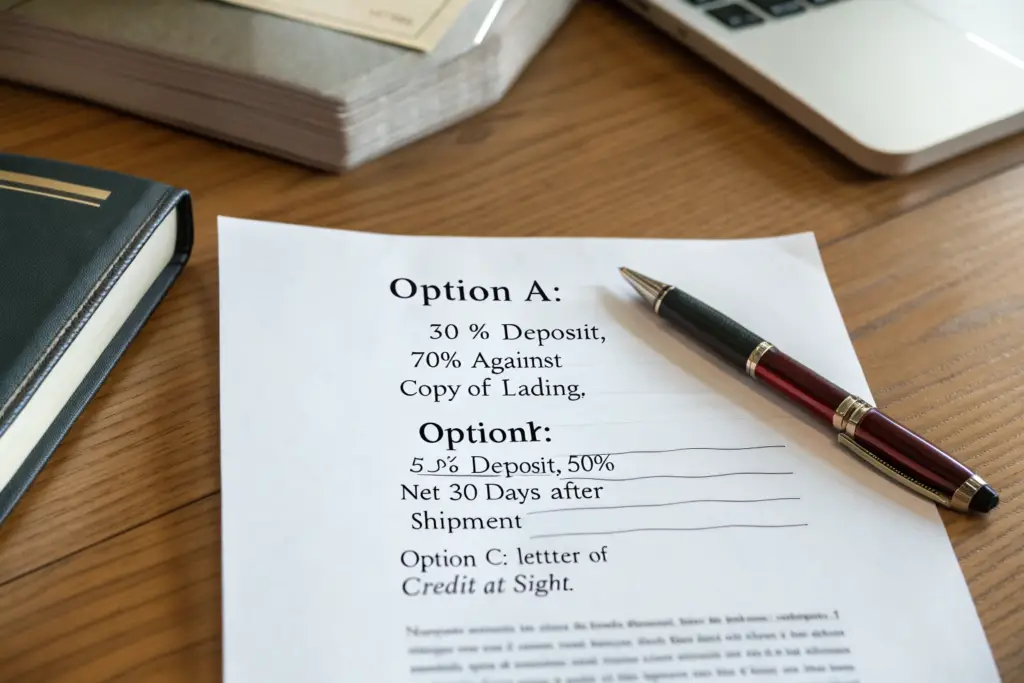

Top-tier Chinese manufacturers typically offer a tiered set of payment structures. The most common for established relationships is a 30% deposit with the 70% balance paid against a copy of the shipping documents or after a passed third-party inspection. For new relationships, the deposit may be 50% to cover the initial risk. Some manufacturers also accept a Letter of Credit at Sight, where the buyer’s bank guarantees payment upon presentation of compliant shipping documents. This is the gold standard for large orders, as it protects both parties. A manufacturer offering Net 30 or Net 60 terms, where the goods ship and the invoice is due 30 to 60 days later, is rare and requires a deep, long-term relationship. These open account terms are the ultimate sign of trust and financial strength from the factory. They signal that the factory has the working capital to finance the production and is confident enough in the relationship to wait for payment.

The payment term a factory offers tells you everything you need to know about their financial health. A factory that can afford to wait 30 days for payment is a factory with a strong balance sheet. A factory that needs your money before they can buy fabric is a factory operating on the financial edge.

What Is the Critical Difference Between “TT Against Inspection” and “TT Against Bill of Lading” for Buyer Protection?

"TT Against Inspection" means the buyer pays the balance after a final quality inspection is conducted and passed. This gives the buyer the right to verify the goods are correct and defect-free before releasing funds. It is the strongest protection for the buyer. "TT Against Bill of Lading" means the buyer pays when the factory presents the shipping document proving the goods have been loaded onto the vessel. The goods may have left port, but the buyer has not yet verified quality. If a problem is discovered upon arrival, the money has already been transferred. The difference is the timing of the quality check. We always recommend buyers negotiate for "TT Against Inspection" or at least a hybrid model where 20% is held back until a third-party inspection report is approved. The Incoterms and payment terms for international trade should be understood by every buyer.

How Can a Letter of Credit (L/C) at Sight Serve as a Perfect Bridge of Trust for a New Wholesale Relationship?

A Letter of Credit at Sight is a bank-to-bank guarantee. The buyer’s bank issues a letter promising to pay the factory the moment compliant shipping documents are presented. The factory knows the payment is guaranteed by a bank, not a small brand they have never worked with. The buyer knows the payment will not be released until the factory proves they shipped exactly what was ordered. The cost is typically 0.5% to 1% of the order value, split between the parties. For a first order of $30,000, the L/C costs $150 to $300 per party. It is the cheapest trust-building tool in international trade. It eliminates the "who goes first" dilemma.

How Does Early Payment Discount Negotiation Create a Win-Win Profit Center for Both Factory and Buyer?

A buyer I work with realized she consistently had cash available in the first week of the month, but her invoices were not due until the 30th. She started offering her suppliers a deal: "I will pay this invoice within 10 days if you give me a 2% discount." For a factory, getting paid in 10 days instead of 60 days is a massive cash flow win. It allows them to pay their own fabric suppliers faster and negotiate their own discounts. The factory agreed. The buyer now saves 2% on nearly every order she places. On $100,000 in annual purchasing, that is $2,000 in pure profit, just for paying early. The factory benefits from predictable, fast cash flow. The buyer benefits from a permanent cost reduction.

Early payment discount negotiation, often structured as "2% 10, Net 30," is a profit center for both parties. The buyer earns a risk-free, tax-free return on their cash that far exceeds any bank interest rate. A 2% discount for paying 20 days early is equivalent to an annualized return of over 36%. The factory receives cash faster, reducing their reliance on bank loans or factoring, and can often negotiate better prices with their own suppliers by paying them early. The key is to frame the negotiation as a partnership, not a squeeze. The buyer should say, "I have the cash available now. If I pay you early, can we share the benefit? You get faster cash, and I get a small discount." This approach builds the relationship rather than damaging it. The factory that agrees to an early payment discount is demonstrating financial literacy and a long-term partnership mindset.

The discount is not a sign that the factory was overcharging. It is a recognition that cash today is worth more than cash in 60 days. Smart factories understand the time value of money and are happy to pay a small fee for faster access to working capital.

What Annualized Return on Cash Does a “2% 10, Net 30” Discount Actually Represent for a Busy Buyer?

The math is compelling. The buyer is paying 20 days early. In exchange, they receive a 2% discount. To annualize this return, you calculate the number of 20-day periods in a year (365 divided by 20 equals 18.25). The annualized return is approximately 2% multiplied by 18.25, which equals 36.5%. This is a completely risk-free return. Compare this to a business savings account earning 4% or the stock market averaging 8% to 10% with significant volatility. The early payment discount is the best use of a buyer’s excess cash. It outperforms almost any other short-term investment available to a small business. The early payment discount return calculation is straightforward and should be evaluated by every buyer.

How Can a Factory Use Early Payments from Buyers to Negotiate Better Raw Material Costs?

A factory that receives cash from buyers in 10 days can negotiate with its fabric mills. The mill typically offers a similar "2% 10, Net 30" discount. The factory takes the buyer’s early payment and immediately pays the mill early, capturing the mill’s discount. The factory’s raw material cost drops by 2%, improving its margin. The buyer’s discount is essentially self-funding. The factory is not losing profit by offering the buyer a discount. It is sharing a portion of the discount it receives from its own suppliers. This creates a virtuous cycle of fast payment and lower costs throughout the supply chain. We practice this at Shanghai Fumao. When our brand partners pay us early, we pay our fabric suppliers early, and everyone’s costs go down.

Conclusion

Highly flexible payment terms are a massive strategic advantage because they transform the buyer-supplier relationship from a cash-constrained transaction into a cash-flow partnership. A buyer who negotiates a low deposit and deferred balance can stock a deeper assortment, test new brands, and protect themselves against late or defective shipments. A buyer who uses early payment discounts can generate a risk-free 36% annualized return on their cash. And a buyer who understands the payment structures offered by top-tier manufacturers can distinguish a financially stable factory from an undercapitalized trading company simply by the terms they offer.

The payment terms are not a minor detail at the bottom of a purchase order. They are the financial architecture of the entire wholesale relationship. The brands and factories that treat payment terms as a strategic lever, rather than a take-it-or-leave-it demand, build partnerships that survive slow seasons, scale during fast seasons, and generate profit for both sides.

At Shanghai Fumao, we offer flexible payment structures designed to align our success with our brand partners’ success. Our standard terms for established partners include a 30% deposit to secure raw materials, with the 70% balance due after a passed third-party inspection. For new partnerships, we accept Letters of Credit at Sight to build mutual trust. For our longest-standing partners, we offer open account terms on a case-by-case basis. We do this because we believe a factory should be financially strong enough to share risk with its buyers.

If you want to discuss payment terms that give your buying strategy more flexibility, reach out to us. At Shanghai Fumao, we are transparent about our financial policies and happy to structure terms that work for both sides. Contact our Business Director, Elaine, at elaine@fumaoclothing.com. She can share our standard payment term options and walk you through the trade finance tools that protect both the buyer and the manufacturer. Your cash is your most valuable asset. Use payment terms to protect it and make it work harder for your business.