You're ready to pay for your first major apparel import order. Your bank offers options, and you hear industry terms: "Just wire the deposit via T/T" or "You should use an L/C for security." But what do these really mean for you, the importer? Choosing between Telegraphic Transfer (T/T) and Letter of Credit (L/C) is not just a technicality—it's a strategic decision that impacts your cash flow, risk exposure, administrative burden, and relationship with your supplier. Understanding the fundamental difference is critical for protecting your capital and ensuring a smooth import process.

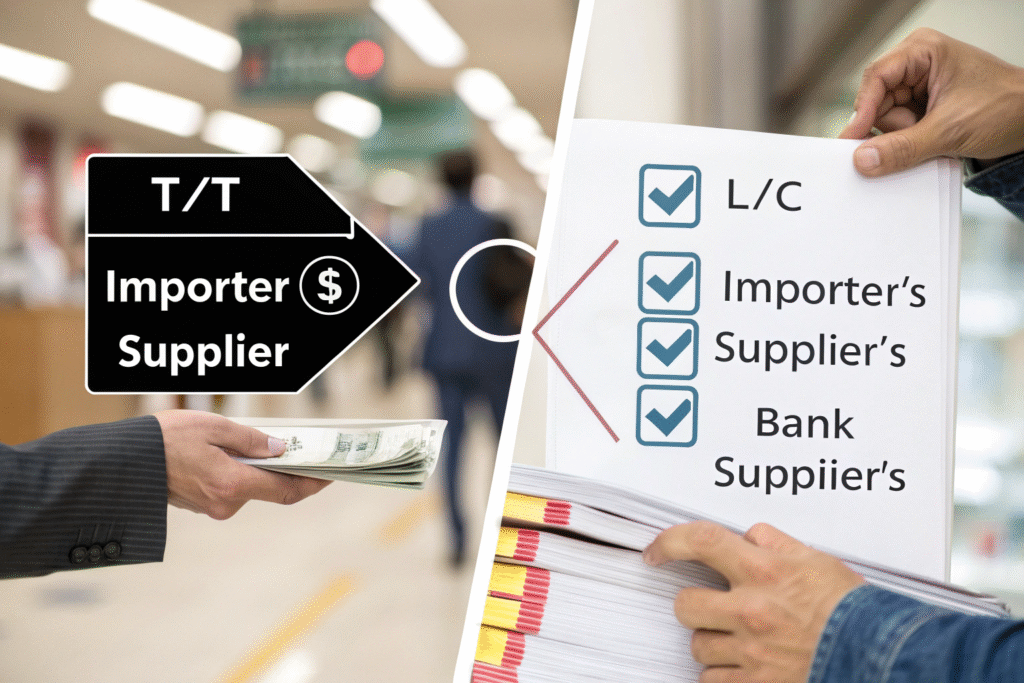

The core difference between T/T and L/C is the party guaranteeing payment and the condition under which funds are released. T/T is a direct, unconditional funds transfer from your bank to the supplier's bank, controlled by you based on trust and agreed milestones. An L/C is a conditional bank guarantee where your bank promises to pay the supplier only upon presentation of perfect shipping and compliance documents, shifting the payment risk from commercial trust to bank scrutiny. For importers, this translates to a trade-off between simplicity/cost (T/T) and documentary security/complexity (L/C).

At Shanghai Fumao, an importer from Canada insisted on an L/C for their first $50,000 order, believing it was the "safest" option. The process consumed three weeks, incurred over $1,200 in bank fees, and was delayed because the Bill of Lading had a minor typo. The shipment was held up. Frustrated, they switched to T/T for their next order. The 30% deposit was sent in 48 hours, production started immediately, and the 70% balance was paid after they approved the inspection report. They saved time, money, and stress. The importer concluded, "The L/C didn't make me safer; it just made everything harder." Let's break down this pivotal choice.

How Does The Fundamental Mechanism Differ?

At their heart, T/T and L/C are built on different principles. One is a payment method; the other is a payment promise facilitated by banks. This foundational difference dictates everything about how they work.

Understanding the mechanism clarifies which risks are being managed—and which are being introduced.

T/T (Telegraphic Transfer): Direct Value Transfer

- The Analogy: Handing cash to someone, but through armored, tracked bank trucks.

- The Process: You (the importer) instruct your bank to send a specific amount from your account directly to the supplier's bank account. Once the funds are sent and received, the transaction is complete. The banks act as conduits, not guarantors.

- Key Characteristic: Unconditional. The payment is not tied to the shipment of goods or any documents. It is based on your commercial agreement with the supplier (e.g., pay 30% now, 70% after inspection).

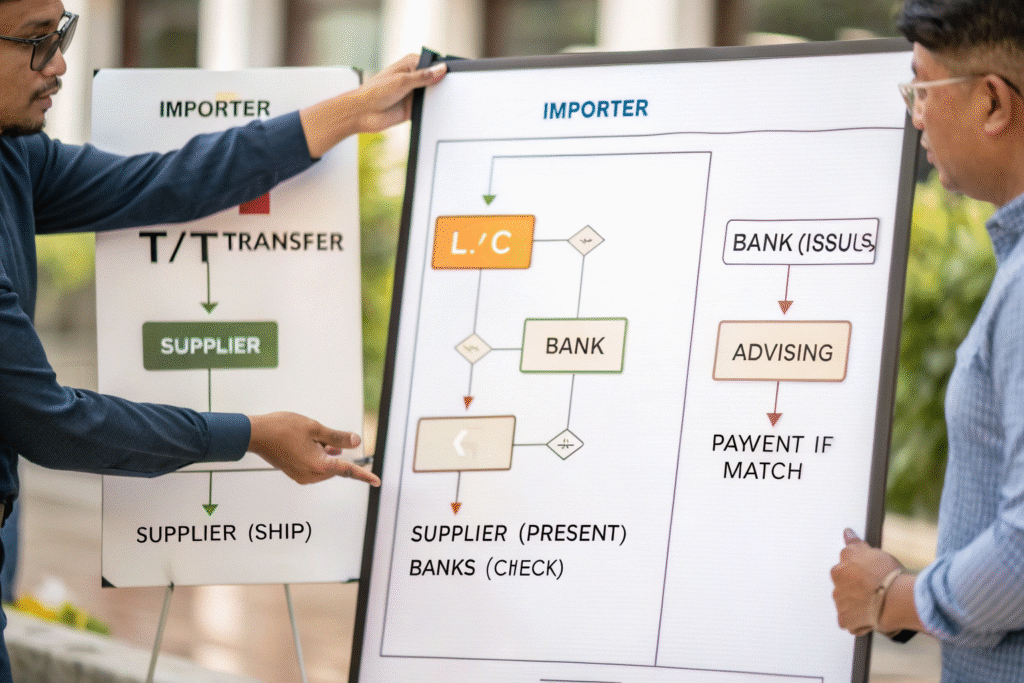

L/C (Letter of Credit): Conditional Bank Guarantee

- The Analogy: Your bank writing a guaranteed cheque that can only be cashed if the supplier presents a pre-agreed set of documents proving they shipped exactly what you ordered.

- The Process:

- You apply to your bank to issue an L/C in favor of the supplier, with extremely detailed terms (description of goods, shipment date, required documents).

- Your bank sends this L/C to the supplier's bank.

- The supplier ships the goods and gathers the documents (Commercial Invoice, Packing List, Bill of Lading, Certificates of Origin, Inspection Certificates, etc.).

- The supplier presents these documents to their bank.

- The banks check if the documents exactly match the L/C terms. If they do, the supplier gets paid. If there's any discrepancy (a "typo," a late shipment, an inconsistent description), the payment can be refused.

- Key Characteristic: Document-Driven. The goods are secondary; the documents representing the goods are primary. Banks deal only in paper, not polo shirts.

This mechanistic difference sets the stage for all subsequent comparisons in cost, time, risk, and control.

What Is The Impact on Cost, Time, and Administrative Burden?

For an importer, the practical implications of cost and time are often the deciding factors. The L/C's "security" comes with a significant operational tax that can strain small to medium-sized businesses.

T/T is designed for agility; L/C is designed for auditability.

Direct Financial Cost Comparison

| Cost Component | T/T (Telegraphic Transfer) | L/C (Letter of Credit) |

|---|---|---|

| Bank Fees | Typically a flat fee per transfer ($25 - $80). | Percentage-based: Opening fee (0.1%-1% of L/C value), advising/confirmation fees, amendment fees, discrepancy fees. |

| Total Cost on a $100,000 Order | ~$100 (for two transfers: deposit + balance). | $1,000 - $3,000+ (1-3% of order value). |

| Hidden Costs | Minimal. | Staff time for document preparation/review, potential wire transfer fees to fund the L/C, cost of delays due to document errors. |

Timeline and Speed Impact

- T/T Timeline: Payment is initiated and typically clears in 1-3 business days. This allows production to start or shipments to be released immediately upon your instruction.

- L/C Timeline: The process adds 2-4 weeks to your financial timeline:

- Application, issuance, and advising: 1-2 weeks.

- After shipment: Supplier prepares documents (3-5 days), banks review (3-7 days). Payment is only released after perfect document review.

In fashion, where selling seasons are short, a 2-week delay in payment (and thus shipment release) can mean missing the market entirely.

Administrative Burden on the Importer

- T/T Administration: You provide bank details and initiate a transfer. The primary admin is verifying the supplier's legitimacy before paying.

- L/C Administration: You are responsible for drafting the L/C application with meticulous, unambiguous terms. You must review and approve documents presented by the supplier's bank. Any mistake in the L/C wording (e.g., "cartons" vs. "boxes") can lead to costly amendments or discrepancies. This requires specialized knowledge or hiring a trade finance specialist.

For most importers, the administrative overhead of an L/C is a significant drain on resources better spent on design, marketing, or sales.

How Does Risk Allocation Differ Between The Two Methods?

Risk management is the central argument for L/Cs. However, it's crucial to understand which risks are mitigated and which new risks are introduced. For importers, the risk profile shifts dramatically.

T&T manages risk through relationship and process control; L/C attempts to manage it through documentary perfection.

Risks MITIGATED by an L/C:

- Supplier Non-Performance / Non-Shipment Risk: The supplier does not get paid unless they ship and present compliant documents. This is the L/C's primary security promise.

- Document Fraud Risk (in theory): Banks are supposed to verify documents. A forged Bill of Lading should be caught.

Risks RETAINED or CREATED by an L/C:

- "Document Discrepancy" Risk: The #1 problem. Banks reject payment for minor typos or technicalities, even if the goods are perfect and shipped on time. You then must decide to waive the discrepancy (accepting flawed docs) or refuse payment, potentially stranding your goods.

- Goods Quality Risk: An L/C does nothing to ensure quality. Banks check paper, not products. The goods could be defective, but if the documents are perfect, the supplier gets paid. You must add a separate Third-Party Inspection Certificate as a required document in the L/C, adding cost and complexity.

- Complexity & Process Risk: The risk of human error in drafting or checking the L/C is high. This complexity itself becomes a source of failure.

- Cost Overrun Risk: The high, often unpredictable bank fees eat into your margin.

Risk Management with T/T:

With T/T, you manage risk through commercial means, which is often more effective for apparel:

- Supplier Vetting: Conduct factory audits, check references, start with a small order.

- Milestone Payments: The 30/70 structure protects you. The 30% deposit is your risk, but it's limited. The 70% is only paid after you verify quality via a Pre-Shipment Inspection (PSI) report.

- Control Through Process: You release final payment, and thus control shipment, only when you are satisfied.

In essence, an L/C transfers commercial risk to documentary risk. For many importers, especially those working with established partners, managing commercial risk through due diligence and controlled payments is simpler and more effective.

In Which Scenarios Is Each Method Most Appropriate?

There is no one-size-fits-all answer. The choice between T/T and L/C should be a strategic decision based on your specific context: the supplier relationship, order value, and your risk tolerance.

Matching the tool to the situation is key.

Favor T/T When:

- Working with Established, Trusted Suppliers: You have a history of successful orders. The relationship itself is the best guarantee.

- Order Values are Low to Medium: The financial exposure is manageable. L/C fees would be a disproportionate cost.

- Time Sensitivity is High: You need to start production or release shipments quickly to meet market deadlines.

- You Have Quality Control in Place: You use inspections (like our in-process QC and final PSI at Shanghai Fumao) to ensure goods meet spec before final payment.

- Simplicity is Valued: Your team lacks specialized trade finance expertise.

This covers the majority of apparel import scenarios.

Consider an L/C When:

- Supplier is New and Unvetted in a High-Risk Context: You are sourcing from a unknown factory in a region with poor legal recourse, and you cannot conduct proper due diligence. (Note: A better first step is often to find a more reputable supplier.)

- Order Value is Exceptionally High (e.g., >$500,000): The absolute financial risk justifies the cost and complexity of the L/C as an insurance policy.

- Your Bank or Investor Requires It: For large financing deals or with certain corporate policies.

- The Goods Are Commodities, Not Custom Apparel: When buying bulk cotton or yarn, where documents perfectly represent the goods, an L/C makes more sense than for complex, custom-manufactured garments.

For most brands importing custom apparel, the L/C's cost and complexity are a solution in search of a problem. The risks it mitigates are better managed through partner selection and process control.

What Are Best Practices for Importers Using T/T?

Given that T/T is the preferred and most practical method, executing it correctly is essential. Following best practices maximizes security and minimizes the inherent risks of direct payment.

Discipline turns T/T from a simple transfer into a robust financial control system.

The Importer's T/T Checklist:

- Vet the Supplier Extensively Before Payment:

- Verify business license.

- Conduct a virtual or physical factory audit.

- Check independent references.

- Start with a small, paid sample development order to test professionalism.

- Use a Detailed, Signed Proforma Invoice (PI): The PI is your payment instruction and should be unambiguous. It should include the supplier's official registered company name and bank details.

- Adhere to Standard Milestone Terms (30/70): This is the industry norm for a reason. It balances risk perfectly. Never agree to 100% upfront.

- Tie Final Payment to Independent Quality Verification: Contractually state that the 70% balance is due only after approval of a Third-Party Pre-Shipment Inspection (PSI) Report. Do not pay the balance blindly.

- Execute Payments Carefully:

- Double-check all bank details against the PI.

- Use the PI or PO number as the payment reference.

- Choose "OUR" for bank charges (you pay all fees) to ensure the supplier receives the full amount.

- Send the bank's SWIFT confirmation to the supplier immediately.

- Build the Relationship: Consistent, on-time T/T payments build trust, which can lead to better terms (like payment against BL copy) in the future.

By following these steps, you leverage the simplicity of T/T while building a secure, transparent, and trustworthy financial workflow with your manufacturer. At Shanghai Fumao, we respect and reward clients who operate this way with priority service and partnership flexibility.

Conclusion

For apparel importers, the choice between T/T and L/C is a fundamental trade-off between agile, cost-effective commercial trust and rigid, expensive documentary security. T/T, with its direct transfer and standard milestone payments, is the preferred instrument because it aligns with the reality of the industry: it is fast, affordable, and when coupled with proper supplier due diligence and quality inspections, provides ample security for the vast majority of transactions.

The L/C, while theoretically offering bank-guaranteed security, introduces high costs, significant delays, and a labyrinth of documentary risk that often outweighs its benefits for custom garment orders. It is a specialized tool for exceptional circumstances, not the default for intelligent importing.

Ultimately, the most secure and efficient supply chain is built not on complex banking instruments, but on strong, transparent partnerships with reputable manufacturers. T/T is the financial mechanism that enables and sustains those partnerships.

If you are seeking a manufacturing partner where transparent T/T terms, rigorous quality control, and a commitment to mutual trust make complex L/Cs unnecessary, we are built for that partnership. At Shanghai Fumao, we operate with the clarity and reliability that allow our clients to pay with confidence using simple, secure T/T transfers. Contact our Business Director Elaine to discuss your next import order: elaine@fumaoclothing.com.