I want to address this topic directly because payment is the moment of maximum anxiety in any overseas sourcing relationship. You’re about to wire thousands of dollars to a factory you’ve never visited, in a country whose legal system you don’t know, to produce goods you won’t see for weeks. That’s not a transaction. That’s an act of trust. And the payment method you choose either protects that trust or exposes it. I’ve been on the receiving end of payments for fifteen years. I’ve seen what works, what creates friction, and what leaves a buyer exposed. I’m Richard, the owner of Shanghai Fumao. In this article, I’ll explain every payment method we accept, the protections and trade-offs of each, and the structure I recommend to first-time clients who are understandably cautious about sending money overseas.

What Is the Standard Payment Structure for Bulk Denim Orders?

The standard structure in our industry has existed for decades, and it exists for a reason. It balances the factory’s need for working capital with the buyer’s need for leverage. I follow this structure for all new client relationships, and I’m transparent about it from the first conversation.

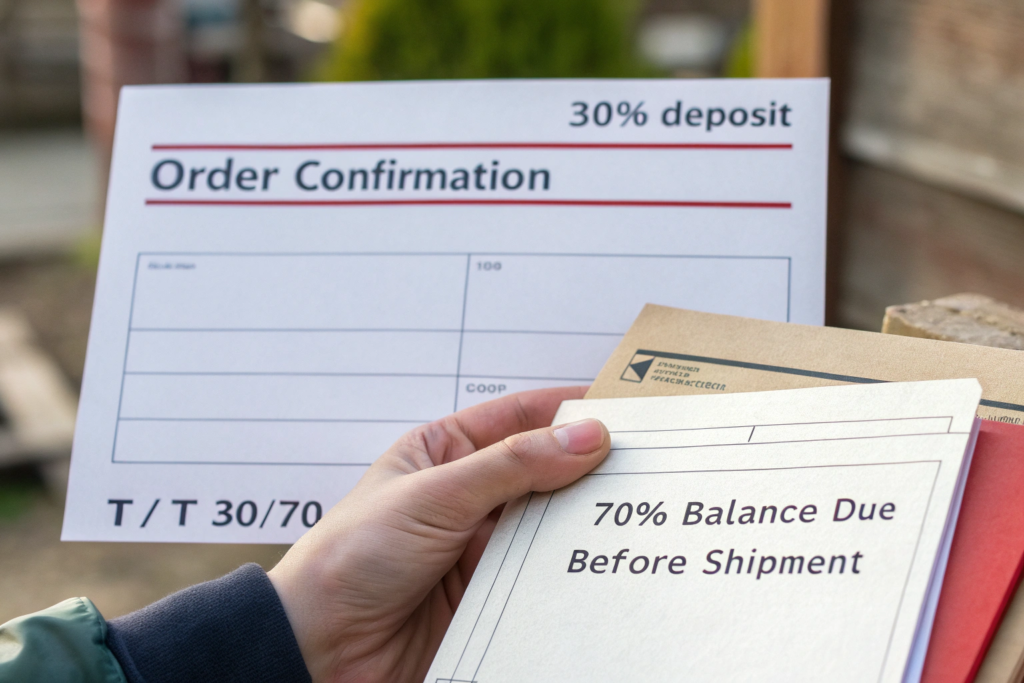

The standard structure is a 30% deposit upon order confirmation, with the remaining 70% balance due before shipment. This is sometimes called T/T 30/70, where T/T stands for telegraphic transfer, the bank wire system that moves money internationally. The 30% deposit covers the factory’s upfront costs: fabric procurement, trim purchasing, and the labor to begin cutting and sewing. These costs are incurred before a single pair of shorts is finished, and the factory needs capital to fund them. The 70% balance is paid when the order is complete, has passed final inspection, and is ready to ship.

The 30% deposit is non-negotiable for new clients. I’ve been asked to start production with a 10% deposit or even no deposit, and I’ve declined. A factory that accepts a very low or zero deposit is either desperate for business—which is its own warning sign—or is building the risk into a higher unit price. Neither is a healthy dynamic. The 30% deposit aligns incentives. The factory has your money and is motivated to produce your order correctly and on time. You have 70% of the payment still in your control, which gives you leverage if something goes wrong.

The 70% balance payment is triggered by the final inspection. Once our QC team completes the AQL inspection and the goods pass, I notify the client. The client reviews the inspection report—which includes photos, measurements, and the defect count—and then releases the balance payment. Only after the balance clears do we release the shipment. Some factories ship on a copy of the wire transfer confirmation, meaning they release the goods as soon as the buyer sends proof of payment. I wait for the funds to land in our account. This is a small protection for the factory, and I’m upfront about it.

For established clients with a history of successful orders, I offer more flexible terms. After three or four orders with on-time payments and no issues, I’m open to discussing a 20/80 split, or even net-30 terms for particularly strong relationships. Payment terms are a reflection of trust, and trust is earned through consistent performance on both sides.

One variation on the standard structure that I offer to startups and small brands is a milestone-based payment schedule. Instead of a single 30% deposit and a single 70% balance, we break the payments into smaller chunks tied to production milestones: 20% at order confirmation, 20% at cutting completion, 20% at sewing completion, and 40% before shipment. This structure reduces the size of each individual payment, which helps with cash flow, and gives the buyer more checkpoints to verify progress before releasing additional funds. The administrative overhead is higher for us, but for a startup placing their first order, the reduced risk is worth the extra paperwork.

How Does the T/T 30/70 Model Protect Both Sides?

The T/T 30/70 model is not perfect, but it’s the least imperfect structure available in an industry where legal contracts are difficult and expensive to enforce across borders. It protects both sides by creating mutual exposure.

For the buyer, the protection is in the 70% holdback. If the factory produces defective goods and refuses to fix them, the buyer can withhold the balance payment. The factory has already spent money on fabric, labor, and trims for the order. If the buyer doesn’t pay the balance, the factory is left with a container of customized shorts that are difficult to sell to another buyer. The factory has a strong financial incentive to resolve the issue and get paid. This leverage is not absolute—a factory that has already been paid 30% might still walk away if the cost of fixing the defects exceeds the value of the balance payment—but it’s meaningful.

For the factory, the protection is in the 30% deposit. A custom denim shorts order is not a commodity. It’s made to the buyer’s specifications: their fabric choice, their wash recipe, their hardware, their labels, their packaging. If the buyer cancels the order after production has started, the factory cannot easily sell those shorts to someone else. The 30% deposit ensures that the factory recovers at least its direct material and labor costs if the buyer defaults. The factory’s risk is the difference between the deposit and the total cost of goods sold. A 30% deposit covers most of that cost for a standard denim order.

The model works because both parties have something to lose. The buyer risks the 30% deposit. The factory risks the 70% balance. Neither party can walk away without pain. This mutual vulnerability is the foundation of the transaction.

There are scenarios where the 30/70 model fails. A factory that is in financial distress might take the 30% deposit and use it to pay other debts, never producing the order. This is why I recommend verifying the factory’s financial stability—through trade references, through platform reviews, through direct conversation—before wiring a deposit. A factory that has been in business for many years, with a track record of successful orders and satisfied clients, is unlikely to risk that reputation for a single deposit. A factory that is new, unknown, and offering unusually low prices is a higher risk.

Can You Negotiate Different Deposit Percentages for Large Orders?

Yes, and this is where the conversation becomes more nuanced. The 30/70 model is a starting point, not an immutable law. For large orders—say, 10,000 units and above—the deposit percentage can often be negotiated downward, because the factory’s risk calculation changes.

On a 10,000-unit order, a 30% deposit represents a substantial sum of money. The factory’s material cost for a large order benefits from volume discounts, so the deposit may exceed the actual upfront cost. In that case, I’m open to a 20% deposit, or even a 15% deposit if the client has a strong credit history with us. The key is that the deposit must still cover the direct material cost. I won’t go below that floor because it would expose me to a loss if the client defaults.

The negotiation should be framed around cost coverage, not around "I want to pay less upfront." A buyer who says, "Let’s calculate your actual fabric and trim cost for this order. I’ll deposit exactly that amount, plus a small buffer, and the balance before shipment," is approaching the negotiation intelligently. They’re acknowledging the factory’s legitimate need for working capital while asking for a deposit that’s calibrated to the actual risk.

For very large orders—20,000 units and above—I sometimes propose a letter of credit instead of a T/T deposit. I’ll discuss letters of credit in a separate section, but they’re worth mentioning here as a negotiation option. A letter of credit shifts the risk from the buyer’s deposit to the banking system, which can be advantageous for both parties on large transactions.

The deposit percentage is also influenced by the product’s resale potential. A standard denim short in a medium stone wash with basic hardware could be sold to another buyer if the original buyer defaults. The factory’s loss is limited. A heavily customized short with unique hardware, a custom wash, and branded labels is much harder to resell. The factory needs a higher deposit to cover the customization risk. I explain this calculus openly to my clients. The deposit is not a punishment. It’s a reflection of the cost I’m incurring on your behalf.

Which Payment Methods Offer the Most Security for Importers?

Security in international payments is about two things: the ability to recover your money if something goes wrong, and the ability to verify that the goods meet your standards before the money is released. Different payment methods offer different levels of protection, and the "most secure" method depends on whether you’re more concerned about supplier fraud or about receiving defective goods.

The payment methods I accept at Shanghai Fumao are, in order of buyer protection from highest to lowest: letter of credit, Trade Assurance via Alibaba, PayPal for sample orders, and direct T/T wire transfer. Each has a different cost, speed, and protection profile.

A letter of credit, or L/C, is the gold standard for buyer protection in international trade. It’s a document issued by the buyer’s bank that guarantees payment to the factory once specific conditions are met—typically, the presentation of shipping documents that prove the goods were shipped as ordered. The bank acts as an intermediary. The factory doesn’t get paid until the bank verifies the documents. This protects the buyer from non-shipment. However, an L/C does not protect against quality issues. The bank checks documents, not products. If the factory ships a container of defective shorts but presents the correct shipping documents, the bank will release payment. The L/C protects against fraud, not against poor quality.

Alibaba Trade Assurance is a platform-based payment protection system. The buyer pays through Alibaba, and Alibaba holds the funds in escrow. The factory ships the order. The buyer confirms receipt and satisfaction, and Alibaba releases the funds. If there’s a dispute—the goods don’t match the contract, the shipment is late, the quality is substandard—Alibaba mediates and can refund the buyer. Trade Assurance is more buyer-friendly than a letter of credit because it covers quality disputes, not just documentation disputes. The downside is that it’s only available for transactions conducted through the Alibaba platform, and it adds a platform fee to the transaction.

PayPal is the simplest and most buyer-protective option, but it’s only viable for small amounts—sample fees, small deposits, initial development costs. PayPal’s buyer protection allows chargebacks if the goods are not as described. The bar for a successful chargeback is relatively low, which makes PayPal risky for the factory. I accept PayPal for sample orders and small development fees, but I don’t accept it for bulk production payments. The chargeback risk is too high.

Direct T/T wire transfer offers the least buyer protection. Once the money is wired, it’s gone. Recovering a wire transfer payment from an overseas factory is extremely difficult, bordering on impossible without legal action in the factory’s home country. T/T is fast, cheap, and simple, which is why it’s the industry standard. But it’s a trust-based method. You wire the money because you trust the factory. I recommend T/T only after you’ve verified the factory’s credentials, visited the factory or done a thorough virtual inspection, and built a relationship.

For first-time clients placing their initial order with Shanghai Fumao, I recommend Alibaba Trade Assurance for transactions under $10,000 and a letter of credit for transactions above $50,000. For the middle range—$10,000 to $50,000—T/T 30/70 is usually the practical choice, balanced by thorough due diligence before the deposit is wired.

![]()

Is a Letter of Credit Practical for Denim Shorts Orders?

The letter of credit has a reputation for being complex and expensive, and that reputation is partially deserved. An L/C involves bank fees on both sides—the buyer’s bank charges for issuing the L/C, and the factory’s bank charges for processing it. The documentation requirements are precise, and a single clerical error in the shipping documents can cause the bank to reject the payment, creating delays and frustration. For a small order, the cost and complexity of an L/C often outweigh the protection it provides.

However, for a large denim shorts order—$50,000 and above—an L/C becomes practical and, in my view, advisable for a first-time relationship. The bank fees, which typically range from 0.5% to 1.5% of the transaction value, are significant in absolute dollars but small relative to the risk they mitigate. On a $75,000 order, an L/C fee of $750 to $1,125 is a reasonable insurance premium against the loss of the entire amount.

The practicality of an L/C also depends on the factory’s willingness to accept it. Some factories refuse L/Cs because they don’t want the documentation burden or because they need faster access to working capital than an L/C provides. A factory that refuses an L/C outright is not necessarily fraudulent, but it’s a data point to consider alongside other information. At Shanghai Fumao, I accept L/Cs for orders above $50,000. The documentation requirements are manageable if both sides have experienced trade documentation staff.

The most common L/C type for denim orders is an irrevocable, at-sight letter of credit. "Irrevocable" means the L/C cannot be changed or canceled without the agreement of both parties. "At sight" means the bank pays immediately upon presentation of compliant documents. This structure gives the buyer the protection of bank intermediation without delaying the factory’s payment beyond the normal shipment timeline.

The documents typically required under an L/C for a denim order include the commercial invoice, the packing list, the bill of lading, the certificate of origin, and any required inspection certificates or compliance documents. The specific document list is negotiated between the buyer and the factory during the L/C setup. I advise buyers to keep the document list simple and to avoid requiring documents that are difficult or expensive to obtain. Every additional document increases the risk of a discrepancy that delays payment.

How Does Alibaba Trade Assurance Protect Your Deposit?

Alibaba Trade Assurance is the most accessible buyer protection tool for small and mid-sized denim orders. It’s integrated into the Alibaba platform, and the process is designed to be straightforward. The buyer places an order on Alibaba with a supplier who offers Trade Assurance. The order specifies the product details, quantity, price, shipping date, and quality standards. The buyer pays through Alibaba’s payment system, and Alibaba holds the funds. The supplier produces and ships the order. The buyer confirms receipt and satisfaction, and Alibaba releases the funds to the supplier.

The protection for the buyer comes from the dispute resolution mechanism. If the goods don’t match the contract specifications—wrong fabric, wrong wash, wrong measurements, late shipment—the buyer can file a dispute. Alibaba’s mediation team reviews the evidence from both sides and makes a determination. If the buyer’s claim is upheld, Alibaba refunds the buyer from the held funds.

The strength of Trade Assurance is that it covers quality and conformity issues, not just non-shipment. A letter of credit only verifies that the shipping documents are correct. Trade Assurance verifies that the actual product matches the contract. This is a fundamentally different and more comprehensive protection.

The limitations of Trade Assurance are the coverage cap and the dispute process. The coverage cap is the maximum amount Alibaba will refund, which is displayed on the supplier’s Alibaba page. If the order value exceeds the cap, the excess is not protected. Buyers should check the cap before placing an order and ensure it covers the full deposit amount. The dispute process, while generally fair, can be slow. A complex dispute with conflicting evidence might take weeks or months to resolve. During that time, the funds are frozen and the goods are in limbo.

I offer Trade Assurance for orders up to the coverage cap on our Alibaba account. For first-time clients placing a sample order or a small trial order, Trade Assurance is the payment method I recommend. It provides the buyer with a safety net while they build confidence in our quality and reliability. After the first successful order, most clients transition to direct T/T for subsequent orders, having established the trust that T/T requires.

What Alternative Payment Solutions Do We Offer for Startups?

Startups and small brands face a payment challenge that large distributors don’t. They need to place small orders—300 to 500 units—to test the market. But many of the traditional payment methods have minimum thresholds that make small transactions impractical. A letter of credit on a $4,500 order doesn’t make sense; the bank fees would eat a significant percentage of the transaction. T/T is simple but offers no protection for a first-time buyer who has never worked with the factory. The startup is caught between methods that are too expensive and methods that are too risky.

I’ve thought a lot about this problem because startups are a significant part of Shanghai Fumao’s client base. As I discussed in a previous article on minimum order quantities, I built our MOQ structure specifically to serve emerging brands. The payment structure needs to match. A startup founder who is investing their personal savings into their first production run deserves payment options that don’t expose them to catastrophic loss.

The solution I’ve developed is a flexible, multi-stage approach that startups can use as they grow. The first stage is PayPal for the sampling phase. The sample fees are small—typically a few hundred dollars—and PayPal provides full buyer protection. The startup founder can pay for samples with confidence, knowing they can recover the payment if the samples never arrive.

The second stage is Alibaba Trade Assurance for the first small production order. If the startup places a 300-unit order at a total value of $3,000 to $4,500, Trade Assurance covers the full amount on our account. The startup has platform-mediated protection for their entire investment.

The third stage is the transition to T/T for subsequent orders. After a successful first order, the startup has a relationship with us. They’ve received product. They’ve verified quality. They’ve experienced our communication and reliability. At that point, T/T becomes a reasonable choice, and it saves the platform fees that Trade Assurance charges.

For startups that need even more flexibility, I offer the milestone-based payment schedule I mentioned earlier. Breaking a $4,500 order into three or four smaller payments tied to production milestones reduces the risk of each individual payment. If something goes wrong, the startup’s exposure at any single point is limited.

Do You Accept PayPal or Credit Cards for Sample Development?

Yes, I accept PayPal for sample development fees and small initial payments. The sample fee covers the pattern making, the sample machinist’s labor, the fabric, and the shipping of the sample to the client. This fee typically ranges from $100 to $300 per sample, depending on the complexity of the design and the wash. PayPal is the ideal payment method for this stage of the relationship.

PayPal’s buyer protection applies to physical goods transactions, which includes garment samples. If the client pays for a sample and the sample never ships, or if the sample arrives and is fundamentally different from what was agreed, the client can file a dispute through PayPal. PayPal’s dispute resolution process is generally faster and more buyer-friendly than bank-mediated processes.

The reason I don’t extend PayPal to bulk production payments is the chargeback risk. PayPal allows buyers to file chargebacks up to 180 days after the transaction. For a bulk production order that takes 30 to 45 days to produce and another 20 to 30 days to ship, a buyer could receive the goods, sell through them, and still file a chargeback claiming the goods were not as described. The factory has no practical recourse once PayPal reverses the transaction. This risk is manageable for a $200 sample. It’s unacceptable for a $20,000 bulk order.

I do not directly accept credit cards for bulk orders, for similar reasons. Credit card chargebacks follow the same buyer-friendly rules as PayPal, and the chargeback window can extend even longer. The factory’s exposure is too high. For sample fees, however, I can process a credit card payment through the PayPal platform if the client prefers to use a card rather than a PayPal balance.

How Do Milestone Payments Work for First-Time Clients?

The milestone payment structure is designed for clients who are placing their first order and want to reduce the size of each individual payment at risk. It breaks the standard 30% deposit into smaller increments tied to production milestones that the client can verify before releasing the next payment.

A typical milestone schedule for a first-time denim shorts order looks like this. Milestone one is the order confirmation payment, which is 15% of the total order value. This payment triggers the fabric procurement and the pattern preparation. The client receives photos of the fabric rolls in our warehouse, with the mill labels visible, and confirmation that the pattern is ready for cutting.

Milestone two is the cutting completion payment, which is another 15%. The client receives photos or a short video of the cut bundles on the cutting table, with the quantity visible. They can see that their fabric has been cut and is ready for sewing.

Milestone three is the sewing completion payment, which is 20%. The client receives photos of the finished shorts on the sewing line, before washing. They can see the construction, the stitching, the overall quality of the unwashed product.

Milestone four is the pre-shipment balance payment, which is the remaining 50%. This is paid after the final QC inspection is complete and the inspection report has been shared with the client. The client reviews the report, confirms they are satisfied, and releases the balance. The goods ship upon receipt of the balance.

Each milestone payment is a smaller amount than the standard 30% deposit, which reduces the client’s financial exposure at each stage. And each milestone is verified with photo or video evidence before the next payment is requested. This structure gives the first-time client multiple off-ramps. If at any stage the product doesn’t meet their expectations, they can pause and address the issue before committing more money.

The milestone structure does extend the overall timeline slightly, because the production pauses at each milestone to wait for client approval and payment. A standard 30-day production run might take 35 to 38 days with milestone pauses. For most first-time clients, the extra week is an acceptable trade-off for the reduced financial risk. After the first successful order, most clients are comfortable transitioning to the standard 30/70 T/T structure for future orders.

How Do We Handle Payment Disputes and Refunds?

Payment disputes in garment manufacturing are almost always about quality. The buyer believes the goods don’t match the approved sample or the contract specifications. The factory believes the goods are within the agreed tolerances. The dispute is about perception, measurement, and contract interpretation. Resolving it fairly requires a clear process, objective evidence, and a shared commitment to finding a solution rather than assigning blame.

My approach to dispute resolution is grounded in the quality documentation that we produce throughout the production process. As I described in a previous article on quality consistency, every order is documented at every stage: the fabric test reports, the inline inspection checkpoints, the wash process control logs, the final AQL inspection report. This documentation provides an objective record of what was produced and how it compares to the approved standard.

When a client raises a quality concern after receiving their order, the first step is to compare the client’s evidence with our internal documentation. The client sends photos of the issue, with measurements if it’s a sizing concern. We pull our QC records for that batch. In most cases, the documentation shows that the goods were within spec when they left our factory, and the client is seeing something different. The issue might be shipping damage, or a misunderstanding of the agreed tolerances, or a subjective perception of color or hand feel that differs from the approved standard.

If the documentation supports the client’s claim—the goods genuinely don’t match the approved sample—we take responsibility. The remedy depends on the severity and the scope of the issue. For a minor, localized defect affecting a small percentage of the order, we issue a credit for the defective units against the next order. For a major, systemic defect affecting a significant portion of the order, we discuss a partial refund or a rework at our cost.

If the documentation supports our position—the goods match the approved sample within the agreed tolerances—we share the documentation with the client and explain why we believe the goods are conforming. This is a difficult conversation, and I approach it with respect. The client is not trying to cheat us. They’re seeing something that concerns them. My job is to explain, with evidence, why the goods meet the standard we both agreed to.

A specific example: a client received a batch of denim shorts and felt the wash was lighter than the approved sample. We pulled the spectrophotometer readings from the production batch and compared them to the readings from the approved sample. The Delta E was 0.8, well within our agreed tolerance of 1.5. The color difference was imperceptible to the human eye under calibrated lighting. We shared the data with the client. They reviewed it, understood the objective measurement, and accepted the batch. The dispute was resolved without acrimony because the data provided an objective foundation.

What Happens If the Goods Don’t Match the Approved Sample?

This is the most serious quality failure, and the response must be proportional and swift. If the goods genuinely don’t match the approved sample—the measurements are outside tolerance, the wash is the wrong shade, the hardware is different from what was specified—the factory is in breach of the production contract.

The first step is to quantify the problem. What percentage of the order is affected? Is the issue cosmetic or functional? Can the goods be sold at a discount, or are they unsellable? The client provides this information, supported by photos, measurements, and if possible, a third-party inspection report from an independent QC company.

The second step is to determine the remedy. If the issue is repairable—loose threads, missing labels, a wash that can be re-processed—we arrange for the goods to be returned to our factory for rework at our cost, or we pay for the rework to be done locally if that’s more practical. If the issue is not repairable—the fabric is the wrong weight, the measurements are fundamentally off—we discuss a refund or a replacement order.

The refund amount is negotiated based on the severity of the issue and the salvage value of the goods. If the shorts are sellable at a discount, the refund might be the difference between the contract price and the discounted selling price. If the shorts are unsellable, the refund might be the full order value. These negotiations are difficult, and they test the factory’s integrity. A factory that values long-term relationships will prioritize a fair resolution over a short-term financial win.

At Shanghai Fumao, I’ve had two instances in the past five years where an order did not match the approved sample to the client’s satisfaction. In one case, the wash had shifted during scale-up from the lab sample to the production batch. We caught it during our internal QC, but the client wasn’t satisfied with the degree of variation. We re-washed the entire batch at our cost. The order shipped two weeks late, but it shipped right. In the other case, a trim substitution had occurred without the client’s explicit approval—a button finish that was slightly different from the approved sample. We had communicated the substitution, but the client hadn’t processed the communication. We shared responsibility. We issued a 5% credit on the order. Both clients are still with us today.

How Do You Issue a Credit or Refund for Quality Issues?

The mechanics of a credit or refund are straightforward, but they vary depending on the payment method used for the original transaction.

For a T/T transaction, a credit is applied against the client’s next order. If the client has a $1,000 credit from a previous order and places a new $10,000 order, the deposit is calculated on $9,000 rather than $10,000. The credit is documented in the purchase agreement for the new order. A refund via T/T is also possible—we wire the agreed amount back to the client’s bank account—but international wire refunds incur bank fees on both sides. Credits are more efficient and are the preferred method for ongoing client relationships.

For an Alibaba Trade Assurance transaction, the refund is processed through the Alibaba platform. The client files a dispute, the parties negotiate or Alibaba mediates, and if a refund is agreed, Alibaba releases the funds back to the client from the held balance. The platform handles the mechanics.

For a PayPal transaction, such as a sample fee, the refund is processed through PayPal’s refund system. It’s instant and fee-free if processed within 60 days of the original transaction.

The important principle is that credits and refunds are agreed upon and documented in writing. A brief email confirming the credit amount and the terms is sufficient for a credit against a future order. A more formal agreement is appropriate for a cash refund. The documentation protects both parties and ensures there’s no ambiguity about what was agreed.

I’ve found that the willingness to issue a fair credit or refund is one of the strongest predictors of a long-term factory relationship. Clients understand that mistakes happen in manufacturing. What they judge is how the factory responds when a mistake occurs. A factory that deflects blame, minimizes the issue, or makes the credit process difficult is a factory that loses the client. A factory that acknowledges the issue, proposes a fair remedy, and implements it quickly is a factory that deepens the client’s trust.

Conclusion

Payment is the culmination of the sourcing process and the foundation of the factory relationship. The method you choose, the structure you negotiate, and the protections you secure will determine whether a production issue becomes a resolvable problem or a financial loss. At Shanghai Fumao, I’ve structured our payment options to accommodate every stage of the client relationship, from the startup placing their first 300-unit order to the established distributor running 10,000-unit programs.

The standard T/T 30/70 model is the industry workhorse for a reason. It balances the factory’s need for working capital with the buyer’s need for leverage. For large orders, a letter of credit provides bank-mediated security, though it protects against documentation fraud rather than quality failure. For first-time and small-volume buyers, Alibaba Trade Assurance offers platform-mediated protection that covers quality and conformity. For sample development, PayPal provides simple, buyer-protected transactions that let both parties test the relationship with minimal risk. And for startups, milestone payments break the order into smaller, verifiable chunks that reduce the financial exposure at each stage.

The common thread across all these methods is transparency. I share our QC documentation at every stage. I provide the evidence that the goods match the approved standard before the balance payment is due. If something goes wrong, I address it with data, not deflection, and I issue credits or refunds that reflect the actual cost of the error. This is not altruism. It’s a business strategy. A client who trusts the payment process is a client who places repeat orders.

If you’re ready to discuss payment terms for a denim shorts order, or if you have questions about which payment method is right for your situation, I encourage you to reach out to our Business Director, Elaine. She can walk you through the options, explain the protections each method provides, and help you structure a payment plan that matches your order size and risk tolerance. You can contact her directly at elaine@fumaoclothing.com. The right payment structure makes the difference between a transaction and a partnership. Let’s build the partnership.