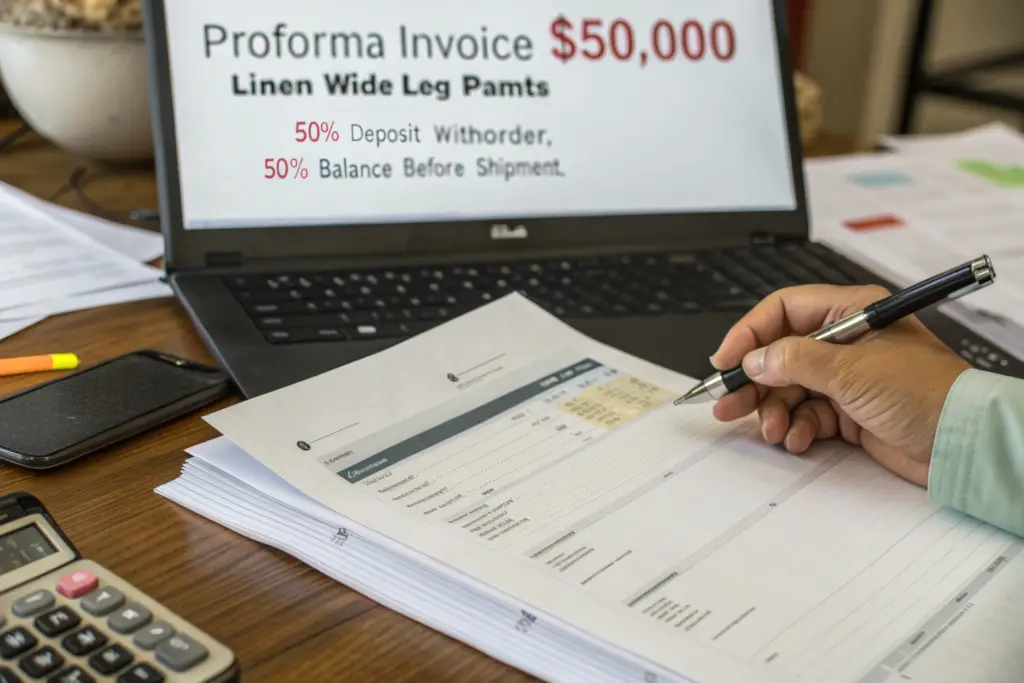

You are ready to place a $50,000 order for linen wide-leg pants. The samples are approved. The delivery date is locked. Then the supplier sends the proforma invoice. The payment terms read: "50% deposit with order, 50% balance before shipment." You feel a knot in your stomach. You have been in this industry long enough to know what that means. Once you wire that final 50%, your leverage evaporates. If the goods arrive with quality issues, you have already paid in full. If the shipment is delayed, you have no financial recourse. The supplier holds all the cards, and you hold a receipt and a prayer. Payment terms are not just a financial detail. They are the primary risk allocation mechanism in your supplier relationship.

To negotiate favorable payment terms on large linen pants orders, you must frame the negotiation around mutual risk reduction, not price pressure. Present yourself as a long-term, high-volume partner, not a one-time buyer. Offer structural alternatives to the standard 50/50 model: a 30% deposit with a 70% balance against a copy of shipping documents, a letter of credit from a reputable bank, or a staged payment schedule tied to verified production milestones. The goal is to retain financial leverage until you have proof—a third-party inspection report, a video of the sealed container, a tracking number—that the goods exist, meet your specifications, and are actually moving toward your warehouse.

My name is Elaine. I am the co-owner of Shanghai Fumao. I sit on the supplier side of the negotiation table every week. I have accepted deposits and I have requested balances. I have also, in my earlier years, felt the temptation to protect my factory’s cash flow by demanding aggressive payment terms. Over time, I learned that the factories that insist on “100% before shipment” are often the ones with the most to hide. The factories that are confident in their quality and their delivery are willing to share financial risk with their long-term partners. In this article, I will explain the logic behind standard Chinese factory payment terms, show you specific, realistic alternatives you can propose, and give you the negotiation language and contract structures that protect your cash without poisoning the relationship.

What Payment Terms Do Chinese Garment Factories Typically Offer, and Why?

To negotiate effectively, you must first understand the factory’s financial reality. A Chinese garment factory is a cash-flow-intensive business. We must purchase fabric from the mill. We must pay for zippers, buttons, and labels. We must pay our workers weekly or monthly. These costs are incurred weeks before we can collect payment from you. The deposit you pay is not profit. It is working capital. It funds the purchase of raw materials for your specific order. Without a deposit, the factory must finance your production from its own reserves or from bank loans, both of which carry cost and risk. This is the legitimate rationale behind upfront payments. It is not greed. It is the cash-flow physics of manufacturing.

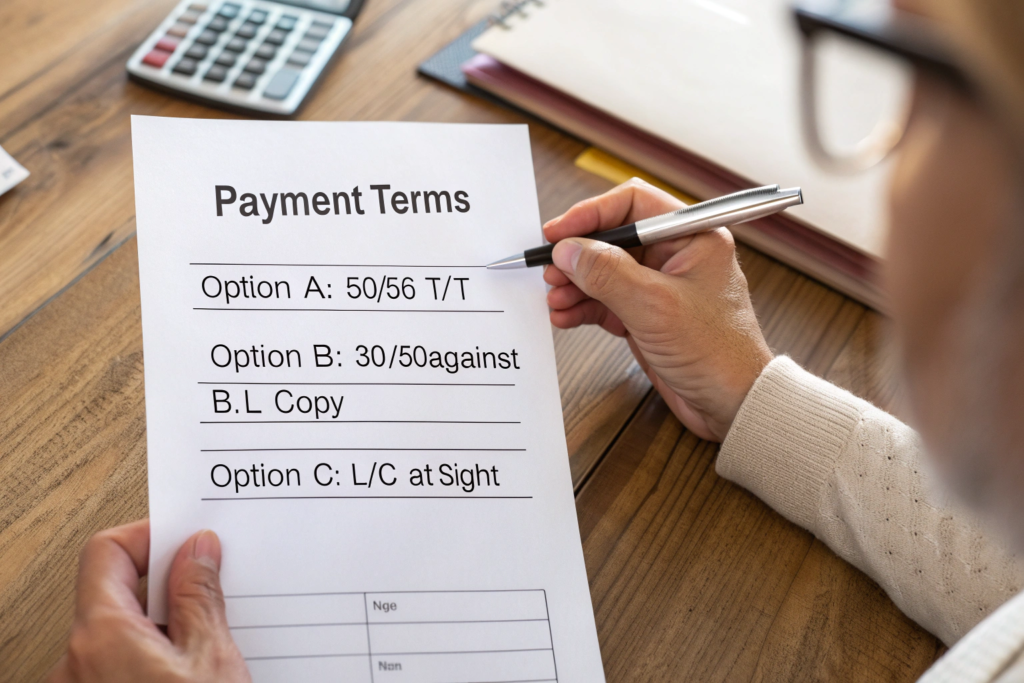

The industry standard for first-time buyers is a 30% to 50% deposit with the purchase order, and a 50% to 70% balance settled before the goods leave the factory. The variation depends on the factory’s assessment of your risk profile as a buyer, the specificity of your order, and the factory’s own working capital position. Understanding that the deposit finances your raw materials, and the balance releases the finished goods, is the key to proposing alternatives that address the factory’s legitimate cash-flow needs while protecting your own financial exposure.

Why Do Factories Demand the Balance Before Shipment?

“Balance before shipment” means the factory wants to receive your full payment before the container leaves their loading dock. From their perspective, this is completely rational. Once the goods are on the water, they lose physical control. If you refuse to pay after receiving the goods, they must pursue an international legal claim that is expensive, slow, and uncertain. A factory that has been burned by a non-paying foreign buyer—and many have—develops a protective instinct. “No money, no goods” becomes a survival rule.

However, this policy transfers all the quality and delivery risk to you. If the goods are defective, you have already paid. If the container is delayed by three weeks, you have already paid. If the supplier substitutes cheaper fabric, you have already paid. Your only recourse is negotiation, which is weak when the other party already has your money. At Shanghai Fumao, our standard terms for new clients are 30% deposit and 70% against a copy of the shipping documents. This means you pay the balance when we provide the bill of lading, the commercial invoice, the packing list, and the third-party inspection report. The goods are at the port. The container is booked. The paperwork proves the shipment exists. You pay, and then we release the original documents or authorize the release of the goods. This structure shares the risk. We have manufactured the goods, so we have incurred the cost. You have not yet received them, so you retain leverage. It is a balanced, fair structure that reflects a partnership of equals. The international trade payment terms guide from the U.S. Department of Commerce explains the risk distribution of various payment methods. The 30/70 against documents structure is the most common compromise between the factory’s need for payment security and the buyer’s need for quality assurance.

What Is a Letter of Credit and When Should You Propose It?

A Letter of Credit is a payment instrument issued by your bank that guarantees payment to the supplier upon presentation of specific, pre-agreed documents that prove the goods were shipped as specified. It replaces the supplier’s trust in you with the supplier’s trust in your bank. It replaces your trust in the supplier with your trust in a set of documents verified by banks on both sides.

For a large order—typically above $30,000—a Letter of Credit can be the ideal instrument. It protects the factory because the bank’s obligation to pay is independent of your willingness to pay. If the documents match the LC terms, the bank pays, even if you are dissatisfied with the goods. It protects you because the bank will not pay unless the documents match exactly. If the supplier ships late, the LC expires and the bank will not pay. If the inspection certificate is missing, the bank will not pay. The documents serve as a proxy for the goods. An LC at sight means the supplier is paid immediately upon presenting compliant documents. An LC at 60 days means the supplier is paid 60 days after presenting documents, giving you a form of short-term trade credit. At Shanghai Fumao, we accept confirmed, irrevocable Letters of Credit from major international banks for orders above $50,000. The LC process requires precision in the documentation, which is a useful discipline for both parties. The Letter of Credit process for importers from the International Chamber of Commerce explains the mechanics. If you are placing a large order and want maximum financial protection, propose an LC at sight. It signals that you are a serious, bankable buyer, and it provides the strongest mutual security available in international trade.

How Can You Structure a Payment Schedule Tied to Production Milestones?

The standard 30/70 or 50/50 payment structure is a blunt instrument. It only has two gates: order placement and shipment. A more sophisticated structure, appropriate for large orders with longer production timelines, ties partial payments to verified production milestones. This approach gives the factory the working capital it needs at each stage of production, and gives you visibility and control at each stage. If a milestone is missed, the payment is delayed. This financial incentive aligns the factory’s behavior with your timeline.

A milestone-based payment schedule for a large linen pants order might be: 20% deposit upon order confirmation to secure fabric, 20% upon submission of a photo of the cut fabric on the cutting table, 30% upon receipt of a passing third-party in-line inspection report during sewing, and 30% against a copy of the shipping documents. Each payment is triggered by verifiable evidence of progress, not a date on a calendar. This structure reduces your exposure at any single point and gives you early warning if production is stalling.

What Milestones Are Verifiable and Meaningful in Garment Production?

Not every production step makes a good milestone. A good milestone is objectively verifiable by you, not just reported by the factory. It represents a genuine commitment of resources by the factory, meaning they have incurred cost that justifies a partial payment. It occurs at a natural decision point where you can intervene if something is wrong.

The first milestone is fabric procurement. The factory must order and receive the bulk fabric. This is a significant cost. You can verify this milestone by requesting a photo of the fabric rolls in the factory’s warehouse, with your order number visible on the roll tags, and a copy of the mill’s delivery note. The second milestone is cutting. The fabric has been spread, marked, and cut. This transforms raw material into work-in-progress. It is the point of no return for the fabric. You can verify this by requesting a photo of the cut pieces on the cutting table, or a short video of the cutting room. The third milestone is an in-line quality inspection. An independent inspector visits the factory during production, examines a sample of semi-finished garments, and issues a report. This milestone confirms that the production quality is on track before the goods are finished and packed. The fourth milestone is the final inspection and shipment readiness. The goods are packed in cartons, the final inspection is passed, and the shipping documents are prepared. You can verify this with the third-party inspection report and a copy of the bill of lading. Each of these milestones is concrete, verifiable, and represents a genuine stage of completion. The garment production milestone tracking guide explains how these stages map to the physical transformation of raw materials into finished goods.

How Do You Propose Milestone Payments Without Offending the Supplier?

A Chinese supplier may initially resist a milestone payment schedule. It feels like micromanagement. It feels like distrust. The way you frame the proposal determines whether it is received as an insult or as a sign of a serious, professional buyer.

Frame the milestone structure as a tool for long-term partnership, not as a response to distrust of this specific supplier. Say, “We use this payment structure with all our long-term partners because it allows us to release payments quickly at each stage of progress. We find it protects the cash flow of both parties. Here is how it worked with our previous supplier.” This language communicates that the milestone structure is a standard operating procedure, not a special condition imposed because you suspect the supplier is unreliable. Also, acknowledge the supplier’s cash flow needs. Say, “We understand the fabric deposit is a significant outlay. We have structured the first payment to cover your fabric cost in full, so you are not financing our raw materials.” This shows that you have thought about their position and designed a schedule that is fair. Offer a slight premium on the unit price in exchange for more favorable payment terms. A $0.30 per unit increase on a 1,000-unit order is $300. In exchange, you gain payment terms that protect tens of thousands of dollars. The math favors you. The supplier feels they have won a concession, which makes the negotiation collaborative rather than adversarial. The cross-cultural negotiation in Chinese manufacturing research explains that saving face and maintaining harmony are as important as the financial terms in Chinese business culture.

What Trade Finance Tools Can Protect Both Parties on Large Orders?

When an order exceeds $50,000 or $100,000, the risk exposure justifies the use of formal trade finance instruments. These tools exist specifically to bridge the trust gap between international buyers and sellers. They are underused by small and mid-sized apparel brands because they seem complex and expensive. They are less complex and less expensive than losing a large shipment. A conversation with your business bank about trade finance options is a sign that you are scaling your business professionally.

The two most accessible trade finance tools for linen pants importers are the documentary Letter of Credit and trade credit insurance. The LC guarantees payment to the supplier upon presentation of compliant shipping documents, protecting them from non-payment risk. Trade credit insurance protects you, the buyer, by covering a percentage of your loss if the supplier fails to deliver the goods as contracted. These instruments convert a bilateral trust relationship into a multilateral, institutionally guaranteed transaction.

How Does Trade Credit Insurance Protect Your Deposit?

Trade credit insurance is a policy you purchase from an insurer that covers your accounts receivable or, in the case of importing, your advance payments to suppliers. If the supplier fails to deliver the goods, delivers goods that are fundamentally non-conforming, or becomes insolvent, the policy pays you a percentage of your loss, typically 80% to 90%. This insurance does not protect against minor quality disputes. It protects against catastrophic failure: the supplier takes your deposit and disappears, or ships goods that are commercially worthless.

The cost of trade credit insurance is a small percentage of the insured value, typically 0.2% to 0.5% for a stable supplier in a moderate-risk country. For a $50,000 order, the premium might be $100 to $250. For that cost, you have insured your deposit and your balance payment against the supplier’s non-performance. This insurance also strengthens your negotiation position. You can tell the supplier, “Our payment is insured. If you deliver as contracted, you will be paid. The insurer provides an independent verification of our financial standing.” This can be a persuasive argument for a supplier who is nervous about extending credit to a new buyer. The trade credit insurance for importers guide from Euler Hermes, a major trade credit insurer, explains the coverage and the application process. Many business banks offer trade credit insurance as an add-on to their business accounts. Ask your bank. The small premium is a reasonable cost for sleeping well at night on a large order.

When Should You Use a Documentary Collection Instead of Open Account?

A documentary collection, often called “Documents Against Payment” or “D/P,” is a middle ground between a full Letter of Credit and an open account. You and the supplier agree that your bank will release the shipping documents to you only after you pay for the goods, or only after you accept a time draft promising to pay at a future date. The supplier ships the goods and sends the documents to their bank, which forwards them to your bank with instructions to release them only upon payment or acceptance.

This mechanism protects the supplier because they retain control of the goods through the documents until payment is made. It protects you because you do not pay until the documents arrive at your bank, and you can review the documents for compliance before releasing payment. It is simpler and cheaper than a Letter of Credit because the banks are acting as document handlers, not as guarantors. The bank does not guarantee payment. It simply holds the documents until the payment condition is met. Documentary collections are governed by the International Chamber of Commerce’s Uniform Rules for Collections. They are a standard, well-understood trade finance instrument. For orders in the $20,000 to $50,000 range, a D/P arrangement can be a pragmatic compromise that provides document-based security without the complexity and cost of an LC. The documentary collection process explained from the U.S. International Trade Administration provides a clear overview of how the process works and when it is appropriate. Propose a D/P arrangement if the supplier is nervous about releasing goods on an open account but an LC feels excessive for the order size.

How Can You Build a Track Record That Unlocks Better Terms Over Time?

The best payment terms—net 30, net 60, open account—are not negotiated in a single meeting. They are earned over a sequence of successful transactions. A supplier who has shipped you five orders, received five on-time payments, and resolved zero disputes, begins to view you as a low-risk, high-value partner. The fear of non-payment that drives aggressive terms fades. The relationship becomes a genuine partnership in which the supplier is willing to extend trade credit because the history proves you are reliable. Your negotiation strategy should include a path to these better terms from the very first conversation.

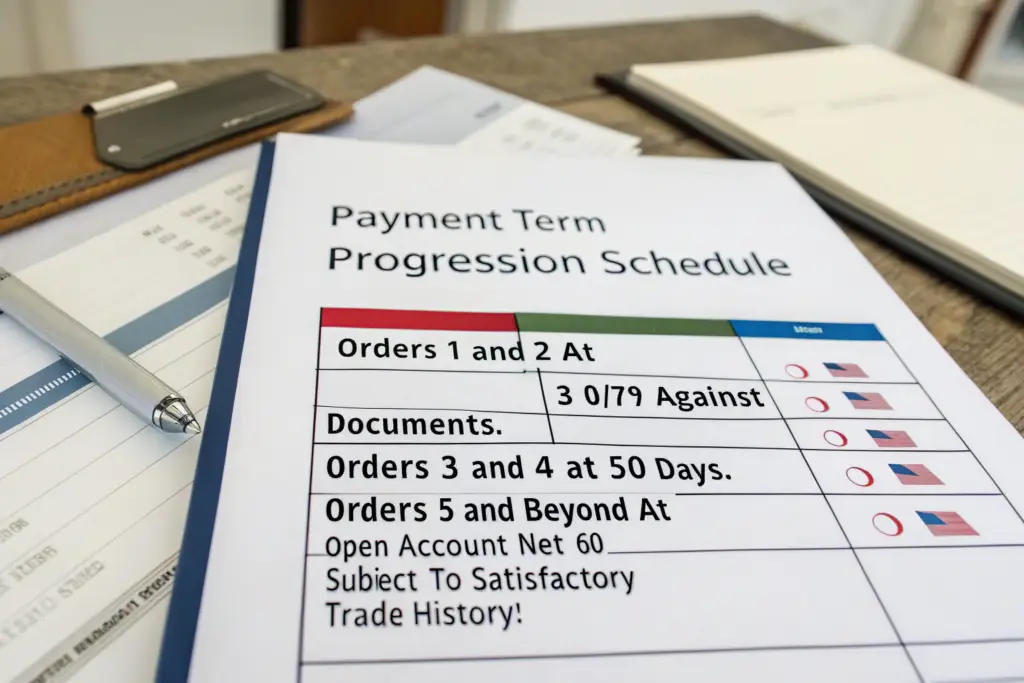

Propose a “payment term progression schedule” at the start of the relationship. For example: “Orders 1 and 2 at 30/70 against documents. Orders 3 and 4 at LC at 60 days. Orders 5 and beyond at open account net 60, subject to satisfactory trade history.” This schedule gives the supplier a clear, predictable path to extending credit, tied to objective performance rather than subjective negotiation. It also gives you a clear incentive to pay on time and build a spotless payment record.

What Does a “Payment Term Progression Schedule” Look Like in a Supplier Agreement?

A payment term progression schedule is a simple table appended to your manufacturing agreement or your first purchase order. It defines the payment terms that will apply to future orders, contingent on the successful completion of previous orders. Successful completion means the goods were delivered within the agreed tolerance of quality and time, and the buyer paid the invoice within the agreed terms.

Here is an example schedule.

| Order Number | Payment Terms | Conditions for Progression |

|---|---|---|

| Orders 1-2 | 30% deposit, 70% against B/L copy | Both orders completed without quality dispute or payment delay. |

| Orders 3-5 | Letter of Credit at 60 days from B/L date | All orders completed with LC terms met. |

| Orders 6+ | Open Account, Net 60 days from B/L date | Review of trade history; supplier may request trade credit insurance. |

This schedule is a commitment from both sides. You commit to a volume of orders that makes the progression worthwhile for the supplier. The supplier commits to a path toward extending credit. It transforms the payment terms from a recurring negotiation into a pre-agreed journey. The supplier can see that your intention is a long-term, high-volume relationship, not a single opportunistic purchase. This visibility into future business often motivates the supplier to accept slightly less aggressive terms on the early orders, because the total value of the relationship is clear. The supplier relationship management and payment terms research confirms that long-term, high-trust relationships achieve more favorable commercial terms for both parties than transactional, bid-based relationships.

Why Is Your Payment Record Your Strongest Negotiating Asset?

In the world of B2B garment sourcing, your payment history is your credit score. A supplier who has received five on-time payments from you values your business far more than a new buyer offering a slightly higher unit price. The certainty of payment, the low administrative burden, and the absence of disputes make you a preferred customer. Preferred customers get better prices, better delivery slots, and better payment terms.

Protect your payment record obsessively. Pay on the exact day the payment is due, not early and not late. Early payment signals that you have loose cash and invites requests for earlier payments. Late payment signals unreliability and justifies tighter terms. Pay exactly on time, every time. Communicate proactively if a payment will be late. A payment that is three days late with a clear explanation given a week in advance damages trust far less than a payment that is one day late with no explanation. After two or three successful orders, politely raise the topic of improved terms. Say, “We have now completed three orders together, all paid within terms. We would like to discuss moving to a Letter of Credit at 60 days for our next order, as a step toward open account terms.” The supplier’s willingness to discuss this is a direct measure of their trust in you. If they agree, you have built a relationship of genuine commercial value. If they refuse without a clear reason, you have learned something important about their risk tolerance and their view of the partnership. The building supplier trust through payment performance guide explains how payment behavior signals creditworthiness in international trade.

Conclusion

Negotiating payment terms for large linen wide-leg pants orders is not a zero-sum game. It is a collaboration to design a financial structure that protects both the factory’s working capital and the buyer’s quality and delivery assurance. The standard 50/50 model is a starting point, not a destination. From that starting point, you can propose a progression of alternatives, each tied to specific, verifiable conditions that reduce the factory’s risk as the relationship matures. A 30/70 against shipping documents retains your leverage until the goods are proved to exist and be on their way. A Letter of Credit replaces personal trust with institutional guarantee, protecting both sides on large transactions. A milestone-based payment schedule aligns cash flow with production progress, giving you visibility and control. And a pre-agreed progression toward open account terms gives both parties a clear path to a low-friction, high-trust partnership.

At Shanghai Fumao, we have structured payment terms across the entire spectrum, depending on the order size, the relationship history, and the client’s preferences. We have accepted 30/70 against documents, confirmed Letters of Credit, and open account terms for long-term partners who have earned that trust. We are willing to discuss payment structures that work for both sides because we measure our success not by one good order, but by ten years of repeat business.

If you are preparing a large order and want to discuss payment terms that protect your investment while ensuring our production runs smoothly, contact me directly. My name is Elaine. My email is elaine@fumaoclothing.com. Share your order volume and your preferred payment structure, and we will work together to find terms that are fair, secure, and partnership-building.